- Healthcare 150

- Posts

- Healthcare M&A 2026: Discipline, Scale, and Strategic Reinvention

Healthcare M&A 2026: Discipline, Scale, and Strategic Reinvention

Why execution, resilience, and AI-driven transformation are redefining dealmaking in a reset market

I. Introduction

Healthcare M&A is not contracting — it is recalibrating.

After a decade shaped by abundant liquidity, aggressive platform roll-ups, and valuation expansion, the industry has entered a more exacting phase. Higher financing costs, valuation dislocations, reimbursement pressure, regulatory scrutiny, and integration fatigue have collectively reshaped the parameters of dealmaking. Transactions are still happening — but the underwriting lens has sharpened.

Capital remains committed to healthcare. Demographic tailwinds, structural labor shortages, digitization across care delivery, and the continued outsourcing of complex services reinforce long-term investment conviction. Few sectors offer the same combination of defensibility, innovation velocity, and secular demand.

Yet the mechanics of value creation have shifted.

The margin for error has narrowed. Integration missteps, physician misalignment, reimbursement volatility, and fragmented technology infrastructure can rapidly erode projected returns in a higher-cost capital environment. Financial engineering alone no longer supports performance. Execution does.

To better understand how market participants are navigating this inflection point, we conducted four targeted micro-surveys, each centered on a defining question:

What will constrain activity most?

Where will resilience concentrate?

What will determine successful transactions?

And how is strategy adapting in real time?

The responses reveal a market defined not by retreat, but by repositioning. Stakeholders are recalibrating sector exposure, deal size, capital structures, and operational playbooks. Risk perception varies by role — investors focus on underwriting durability, operators prioritize physician engagement, clinicians demand economic clarity, and dealmakers emphasize technology integration.

At the same time, macro data shows that while transaction volumes have moderated, deal values are rebounding — driven by larger, more strategic bets. The cycle is not about activity for its own sake. It is about precision, scale, and structural positioning.

Healthcare M&A is not in decline. It is in transition.

The defining feature of this phase is not volume — it is discipline.

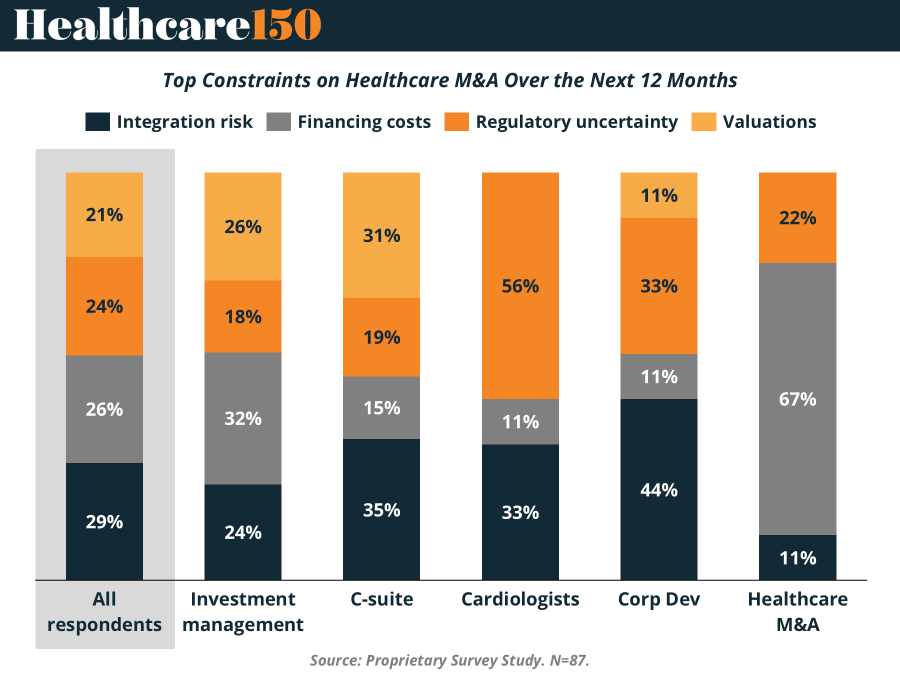

II. What Will Really Slow Healthcare M&A in the Next 12 Months?

Healthcare dealmaking isn’t short on capital — or targets. What it is short on is certainty.

Our micro-survey responses reveal something more nuanced than the usual headline explanations. While valuations and regulation dominate public narratives, the true constraint on healthcare M&A depends heavily on stakeholder perspective. The result is a fragmented environment where risk perception — not lack of appetite — is shaping transaction velocity.

Integration Risk: The Quiet, Structural Drag

Across respondents, integration risk stands out as the most structurally consistent concern. Nearly 30% identify post-close execution as the primary constraint on activity — ahead of pricing and regulatory issues.

This reflects lessons from the last consolidation cycle. Acquiring assets proved straightforward. Integrating them did not.

Clinical workflow harmonization, EHR interoperability, physician incentive alignment, compliance integration, revenue cycle coordination — each adds complexity. When margins are tighter and leverage is more conservative, the tolerance for integration missteps declines sharply.

This concern is especially pronounced among corporate development teams, where 44% cite integration risk as their main bottleneck. For strategics, the question is no longer whether to acquire — but whether the organization can absorb incremental scale without operational dilution.

In this cycle, execution capacity is a gating factor.

Financing Costs: A Capital Markets Reality Check

Although rate volatility has moderated, financing costs remain the dominant constraint among Healthcare M&A professionals. A striking 67% identify capital costs as the primary limiting factor.

This divergence is important. It suggests:

Leverage assumptions are still being recalibrated

Deal structures are becoming more conservative

Smaller platforms and roll-up strategies feel disproportionate pressure

Sponsors and deal teams are underwriting more cautiously, often prioritizing cash flow durability over growth narratives. The weighted average cost of capital has risen, and return thresholds have adjusted accordingly.

Interestingly, financing costs rank lower among clinicians and operating executives. That gap highlights a growing tension between strategic ambition and capital feasibility.

Regulatory Uncertainty: Front and Center for Clinicians

For provider-led respondents — particularly cardiologists — regulatory uncertainty is the leading concern, with 56% identifying it as the main brake on activity.

From their vantage point, risk is immediate and operational:

Reimbursement volatility

Antitrust scrutiny

Scope-of-practice dynamics

Payer contracting pressure

Regulatory enforcement cycles feel less predictable, and scale can attract attention. For clinical leaders, M&A is not purely financial — it can directly affect care models, compensation structures, and compliance exposure.

In their view, growth must not come at the expense of operational stability.

Valuations: A Factor, But Not the Decider

Despite multiple resets over the past two years, valuations are no longer the primary obstacle. Across most respondent groups, pricing ranks behind execution, financing, and regulation.

For C-suite leaders, valuations matter — but context matters more. Integration remains their top concern, followed by pricing discipline. In other words, executives are willing to pay for assets that align operationally and strategically. They are less willing to overpay for assets that introduce complexity without clear synergies.

The market is selective — not frozen.

The Bottom Line

Healthcare M&A is not constrained by lack of ambition. It is constrained by risk asymmetry.

Operators worry about integration

Deal teams worry about financing

Clinicians worry about regulation

Executives balance all three

The common thread is confidence — specifically, confidence in what happens after close.

The acquirers that succeed over the next 12 months will not simply source attractive assets. They will underwrite execution rigorously, structure capital creatively, and anticipate regulatory friction before it surfaces in diligence.

In this environment, the limiting factor isn’t appetite. It’s conviction in post-deal performance.

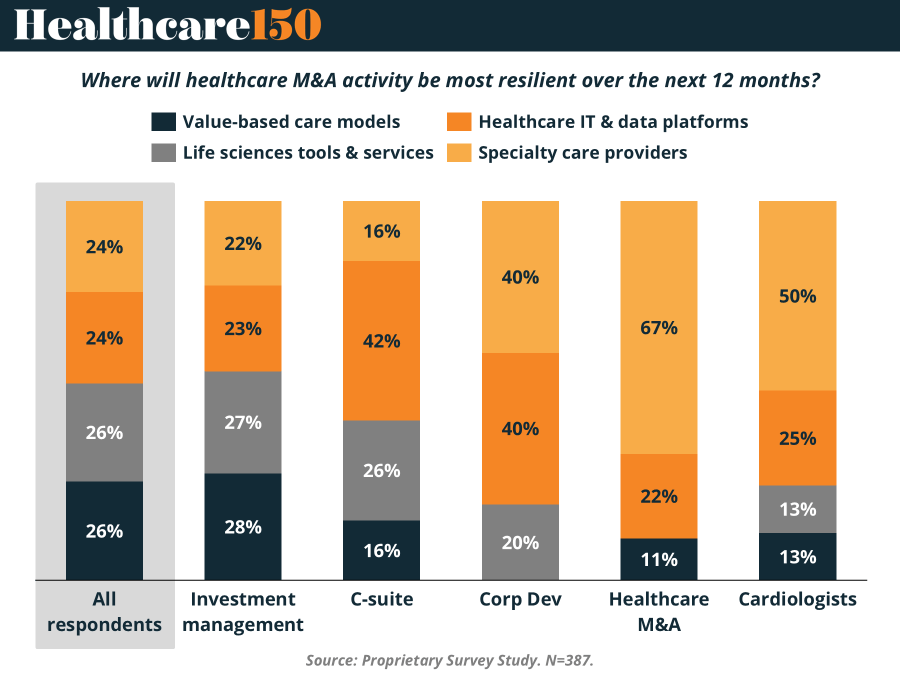

III. Where Healthcare M&A Is Most Likely to Hold Up in 2026

Healthcare M&A may be slower and more selective, but it is far from stalled. The latest microsurvey responses suggest that capital is not retreating from the sector — it is concentrating. Investors and operators are reallocating toward areas where cash flow visibility, scalability, and regulatory defensibility remain strongest.

When asked where healthcare M&A activity will be most resilient over the next 12 months, four themes emerged: healthcare IT & data platforms, specialty care providers, value-based care models, and life sciences tools & services.

No Clear Leader Across the Full Sample

At the aggregate level, responses are remarkably balanced. Value-based care models and life sciences tools & services each capture 26% of responses, while healthcare IT & data platforms and specialty care providers follow closely at 24% each.

This even distribution reflects a market that is cautious but active. Rather than chasing a single dominant narrative, participants appear to be underwriting resilience based on fundamentals — revenue durability, reimbursement exposure, integration complexity, and margin stability.

In other words, there is no broad-based thematic rush. There is selective conviction.

Specialty Care Gains Conviction Among Deal Practitioners

The picture sharpens when isolating respondents closest to transaction execution and clinical operations. Among healthcare M&A professionals, 67% expect specialty care providers to be the most resilient segment. Half of cardiologists share that view.

This conviction is rooted in structural characteristics:

Procedure-driven revenue models

Outpatient migration tailwinds

Fragmented provider landscapes

Platform consolidation potential

In a more disciplined environment, specialty care offers near-term cash flow durability combined with scalable roll-up opportunities. For operators on the ground, it represents controllable growth rather than thematic speculation.

Healthcare IT & Data Platforms Lead with Executives

Among C-suite respondents, healthcare IT & data platforms stand out. 42% of senior decision-makers identify IT and data assets as the most durable M&A target over the next year.

Corporate development teams echo this perspective, with 40% selecting healthcare IT & data platforms — tied with specialty care providers.

The rationale is strategic. Software-enabled assets improve efficiency, support interoperability, enhance data analytics, and often generate recurring revenue streams. As providers and payers continue prioritizing cost containment and digital transformation, scalable technology platforms offer operational leverage without the same reimbursement exposure faced by clinical assets.

For corporate buyers, these acquisitions are not purely financial — they are infrastructure investments.

Value-Based Care Remains in Play — with Tighter Underwriting

Value-based care models continue to attract interest, particularly among investment managers, where 28% expect resilience. However, enthusiasm appears more measured compared to prior cycles.

The signal is clear: value-based care is transitioning from narrative-driven expansion to performance-driven selectivity. Proven payer alignment, demonstrated cost savings, and disciplined unit economics now matter more than growth projections alone.

Capital remains available — but underwriting standards have tightened.

Life Sciences Tools & Services Offer Defensive Stability

Life sciences tools & services maintain steady support across respondent groups. While not viewed as the most aggressive growth vector, these assets benefit from long-term secular demand, recurring utilization patterns, and diversified end markets.

In a higher-cost capital environment, they represent defensive stability within healthcare M&A portfolios — less sensitive to reimbursement shifts and more insulated from provider consolidation risk.

What This Signals for 2026

The resilience story in healthcare M&A is not about a single dominant subsector. It is about differentiated conviction.

Operators and deal teams gravitate toward specialty care for execution certainty and consolidation potential.

Executives and corporate buyers prioritize healthcare IT and data platforms for efficiency and scale.

Investors remain selectively engaged in value-based care and life sciences tools, applying more rigorous underwriting standards.

The next 12 months are unlikely to reward breadth. They will reward precision. Capital will flow toward assets that combine durable demand, defensible economics, and realistic integration pathways — not just thematic appeal.

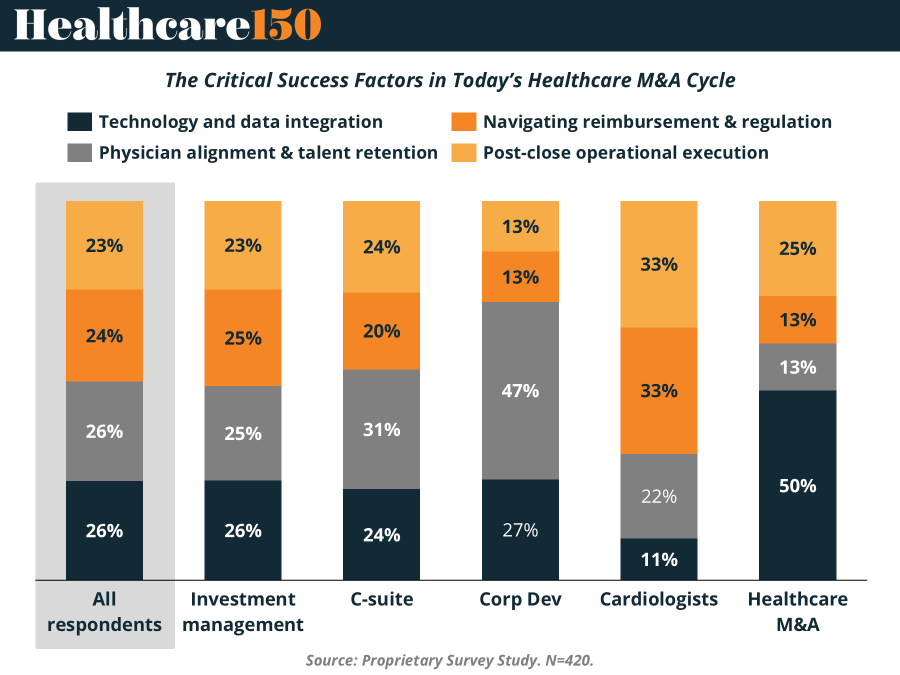

IV. What Will Matter Most for Successful Healthcare M&A in This Cycle?

In a market shaped by higher capital costs, tighter underwriting standards, and elevated regulatory scrutiny, healthcare M&A is no longer just about identifying the right asset. The defining question is what happens after the deal closes.

To understand where success or failure will hinge, we asked 420 investors, operators, corporate development leaders, and clinicians a single question: What will matter most for successful healthcare M&A in the current cycle?

The answers reveal a market where complexity — not capital — is the central challenge.

No Single Bottleneck — A Multi-Front Execution Test

At the aggregate level, responses are almost evenly distributed:

Technology and data integration (26%)

Physician alignment and talent retention (26%)

Navigating reimbursement and regulation (24%)

Post-close operational execution (23%)

That near-perfect balance is telling. This cycle is not defined by one dominant constraint. It is defined by interconnected operational risks. Success requires simultaneous strength across technology, talent, reimbursement navigation, and execution discipline.

Healthcare M&A has become multidimensional.

Investors: A Three-Sided Risk Equation

Among investment professionals, concerns cluster around a three-part equation: technology integration, physician alignment, and reimbursement pressure all rank nearly equally.

This reflects how underwriting has evolved. Margin sustainability now depends as much on retaining clinical talent as it does on integrating systems or protecting payer economics. In a higher-rate environment, operational friction has a more direct impact on returns. Assumptions around productivity, churn, and integration timelines carry greater sensitivity than they did during the low-cost capital era.

For investors, execution risk has moved to the center of the model.

Operators: Physician Alignment as the Decisive Factor

Inside operating organizations, the signal becomes clearer.

Among C-suite leaders, physician alignment and talent retention (31%) emerges as the top priority. Corporate development teams are even more decisive, with 47% identifying physician alignment as the single most important success factor.

This is a critical insight. For those closest to integration, the primary risk is human capital. If physicians disengage, reduce productivity, or exit, value creation deteriorates immediately. In roll-up strategies particularly, retention risk quickly becomes valuation risk.

In this cycle, alignment is not a cultural issue — it is a financial one.

Clinicians: Reimbursement Stability and Operational Clarity

Cardiologists in our survey offer a different lens. They split their top concern evenly between navigating reimbursement (33%) and post-close operational execution (33%), while placing significantly less emphasis on technology integration (11%).

From the clinical perspective, economic stability and workflow clarity outweigh systems architecture. Physicians want reassurance that revenue cycle performance will improve — not deteriorate — and that operations will become simpler, not more bureaucratic.

Technology is valuable only if it translates into tangible clinical and financial benefits.

Deal Professionals: Technology as the Connective Tissue

Healthcare M&A professionals lean heavily toward technology and data integration (50%) as the defining factor for success.

This reflects a broader structural shift. As margin compression intensifies and value-based models expand, the ability to integrate EMRs, unify analytics, and generate actionable insights becomes a strategic differentiator. Data capabilities increasingly shape cost control, clinical optimization, contracting leverage, and scalability.

Technology is no longer a support function. It is a core value driver.

The Structural Takeaway

Viewed together, the responses reinforce a fundamental shift in healthcare M&A.

Investors are underwriting operational durability.

Operators are prioritizing physician engagement.

Clinicians are demanding reimbursement stability and smoother execution.

Dealmakers see technology as the system that binds it all together.

This is no longer primarily a capital markets exercise. It is an execution cycle.

In today’s environment, value is not created at signing. It is created — or destroyed — in the months that follow.

V. The 2026 Acceleration: Reinvention, AI, and the Race for Resilience

If the survey responses reveal how stakeholders are managing risk, broader industry signals show something equally important: healthcare M&A is shifting from defensive positioning to strategic reinvention.

Health industries leaders are entering 2026 with renewed urgency. After two years dominated by macro volatility, pricing pressures, and regulatory headwinds, the tone is no longer cautious stabilization — it is selective acceleration.

Four structural forces are reshaping the deal landscape:

1. Resilience as a Strategic Filter

Buyers are increasingly prioritizing assets defined by high-quality innovation, durable margins, recurring revenue models, and differentiated data. In a higher-cost capital environment, resilience is no longer a defensive trait — it is a prerequisite for valuation support.

This reinforces what surfaced in our survey: execution and integration matter because fragile business models cannot absorb operational friction. Capital is flowing toward platforms that can withstand reimbursement pressure and regulatory variability without sacrificing growth.

2. Value Creation and Exit Readiness

Both corporates and financial sponsors are preparing for potential exit windows that could reopen quickly. That is shifting the focus toward assets that demonstrate scalable value creation levers — not just revenue growth, but margin expansion, AI-driven productivity, and portfolio repositioning.

M&A is increasingly being used to accelerate capability-building rather than simply expand footprint. Divestitures are rising alongside acquisitions as companies reshape portfolios for sharper strategic focus.

3. Consumerisation and Tech-Enabled Care

Healthcare delivery is becoming more data-driven, automated, and patient-centric. AI, interoperability, and digital infrastructure are no longer peripheral upgrades — they are redefining care pathways.

By 2035, more than $1 trillion in global healthcare spending is projected to shift toward prevention, personalized care, home-based services, and digital ecosystems. That shift is already influencing today’s deal logic. Assets that enable care-anywhere models, data analytics, automation, and patient engagement are attracting strategic premium.

This macro trend complements the survey insight that technology integration is increasingly viewed as central to M&A success.

4. Global Rebalancing of Innovation

Innovation leadership is broadening beyond traditional US and European hubs. China and other emerging research ecosystems are scaling discovery capabilities, creating new cross-border partnership opportunities and competitive pressures.

As innovation globalizes, cross-border transactions and strategic partnerships are likely to become more important components of portfolio strategy.

M&A as the Catalyst for Reinvention

In 2026, M&A is not merely a growth tool — it is the fastest route to business model transformation.

Across biopharma, medtech, health services, and digital health, transactions are being used to:

Modernize operations

Accelerate scientific and digital capabilities

Embed AI-driven efficiencies

Reposition portfolios toward prevention-led and personalized models

Data-driven diligence, AI-enhanced integration, and disciplined execution will increasingly differentiate leaders from laggards.

If the previous cycle rewarded speed and scale, the next phase will reward conviction and strategic clarity. The companies that act early, transact with purpose, and integrate technology into the core of operations will be best positioned to shape the next era of healthcare.

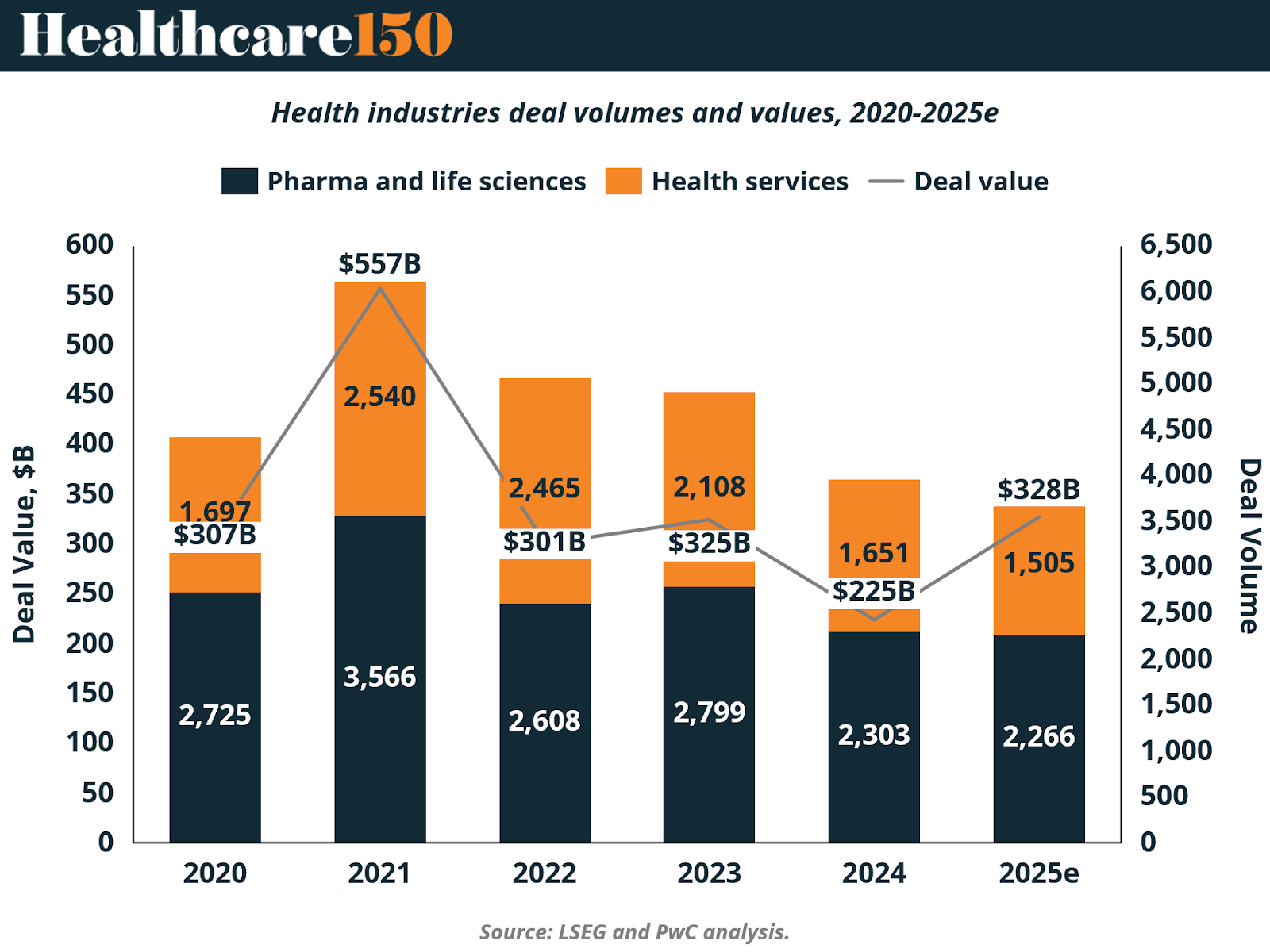

VI. Deal Values Surge as Volumes Normalize

While stakeholder sentiment reflects caution and execution discipline, the aggregate data tells a more nuanced story: healthcare M&A is regaining financial momentum — even if transaction counts remain subdued.

In 2025, global health industries deal values rose 46%, despite a 5% decline in overall deal volume. The rebound was not broad-based in count, but concentrated in scale. Eleven megadeals (transactions above $5 billion) closed during the year — up sharply from just three in 2024.

The implication is clear: capital is consolidating into larger, more strategic transactions.

From Volume Expansion to Value Concentration

The chart illustrates the arc of the cycle:

2021 marked the post-pandemic peak, with $557B in deal value and elevated volumes across pharma, life sciences, and health services.

2022–2024 reflected recalibration — volumes moderated and deal values compressed as financing conditions tightened.

2025 shows a structural shift: volumes remain below peak levels, but value has rebounded to $328B, driven by larger, high-conviction transactions.

This divergence reinforces a central theme of the current cycle: fewer deals, but bigger bets.

Regional Divergence Signals Strategic Reallocation

Beneath the global figures, regional dynamics are diverging.

Asia Pacific recorded the strongest growth in deal volume, up 12% year over year.

EMEA saw modest expansion of 5%.

The Americas experienced a 23% decline in deal count.

However, the Americas continue to dominate in value terms, accounting for nearly two-thirds of total global deal value and nine of the eleven megadeals.

Much of Asia Pacific’s volume growth was driven by a 53% surge in China dealmaking, as investors targeted the country’s expanding innovative drug development ecosystem. This aligns with the broader global rebalancing of innovation discussed earlier — capital is increasingly following R&D capability.

What the Data Suggests

The recovery in aggregate deal value, coupled with lower transaction volume, suggests a more polarized market:

Strategic acquirers are deploying capital decisively when conviction is high.

Financial sponsors are concentrating on platform-defining or capability-building assets.

Regional growth patterns reflect shifts in innovation geography and capital flows.

The 2025 rebound does not signal a return to the liquidity-driven expansion of 2021. Instead, it points to a market entering 2026 with renewed confidence — but sharper selectivity.

If the prior phase was about breadth, the current phase is about scale, strategy, and structural positioning.

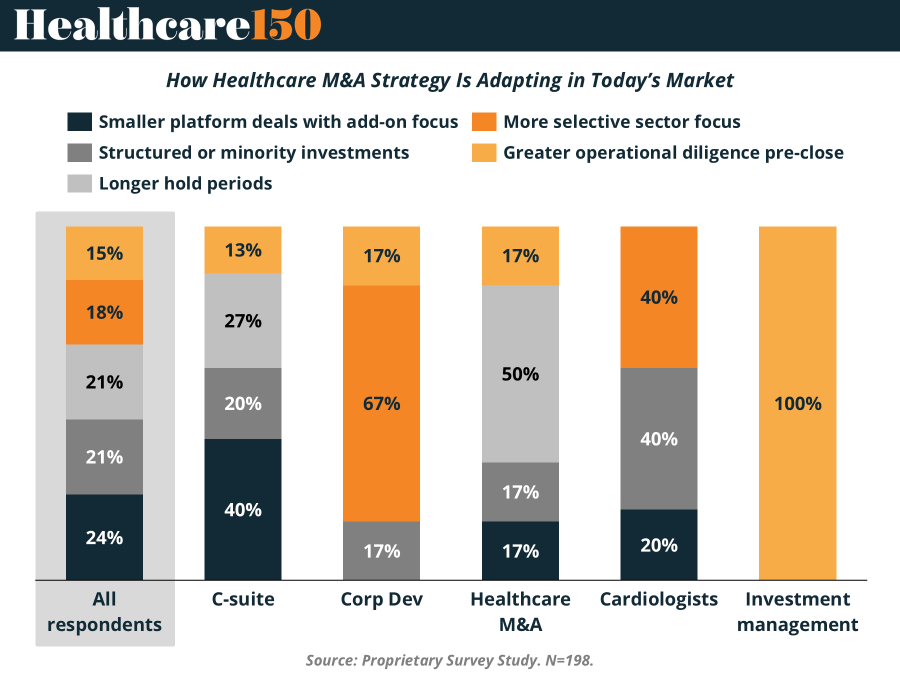

VII. How Healthcare M&A Strategy Is Adapting in the Current Environment

Healthcare dealmaking has not slowed because capital disappeared — it has slowed because the rules of engagement have changed.

In our latest Healthcare 150 proprietary microsurvey, investors, operators, and corporate development leaders indicate that rising capital costs, valuation uncertainty, and operational complexity are reshaping how transactions are structured and executed. Rather than pursuing aggressive platform expansion, buyers are increasingly prioritizing discipline, operational visibility, and sector expertise before committing capital.

The result is a clear evolution in the healthcare M&A playbook.

Smaller Platform Deals with Add-On Focus

The most common strategic shift is toward smaller platform acquisitions followed by targeted add-on deals, cited by 24% of respondents overall and 40% of C-suite leaders. Instead of building scale through large, high-risk transactions, buyers are increasingly adopting a staged approach: acquire a manageable platform, integrate operations carefully, and expand through bolt-on acquisitions that strengthen capabilities or geographic reach.

In a higher-cost capital environment, this approach allows sponsors to de-risk integration while maintaining a path to scale. Operational improvements and margin expansion — rather than valuation multiple expansion — become the primary drivers of value creation.

Structured and Minority Investments

Deal structures are evolving as well. Structured or minority investments account for 21% of responses, reflecting a growing preference for flexible capital deployment.

These structures allow investors to maintain exposure to attractive healthcare assets while limiting downside risk and preserving optionality. Minority stakes, joint ventures, and structured equity arrangements are increasingly used when valuation expectations remain wide or when operators prefer to retain control while accessing growth capital.

In today’s environment, capital providers are seeking participation without overexposure.

Greater Operational Diligence Before Close

Perhaps the most significant shift is occurring in the diligence process itself. Greater pre-close operational diligence was cited by 50% of healthcare M&A specialists, underscoring the increasing complexity of evaluating provider economics, reimbursement stability, and workforce dynamics.

Among investment management respondents, the signal is even stronger: 100% indicated deeper operational diligence before committing capital. Investors are scrutinizing revenue cycle performance, physician productivity, payer mix, and regulatory exposure with far greater intensity than in previous cycles.

Financial engineering alone is no longer sufficient. Operational performance assumptions now sit at the center of underwriting models.

Longer Hold Periods

Longer hold periods — also cited by 21% of respondents — reflect a shift in expectations around value realization. With exit markets less predictable and leverage less abundant, sponsors are increasingly planning for extended ownership horizons.

This allows investors to focus on operational transformation, technology integration, and margin improvement rather than relying on short-term multiple expansion. In many cases, longer holds also align with the gradual platform-building strategies emerging across the sector.

More Selective Sector Focus

Finally, buyers are becoming far more selective about where they deploy capital. Corporate development leaders overwhelmingly highlighted a more targeted sector focus (67%), signaling that organizations are concentrating resources in subsectors where they possess deep operating expertise and clearer demand visibility.

Rather than spreading capital broadly across healthcare services, buyers are focusing on areas where they understand reimbursement structures, integration pathways, and operational levers.

This increasing specialization reinforces a broader trend seen throughout the report: precision is replacing breadth.

The Strategic Takeaway

Taken together, these shifts illustrate how healthcare M&A strategy is evolving in response to a more disciplined market environment.

Investors are still deploying capital — but the methods have changed. Deals are becoming smaller, more structured, more operationally scrutinized, and more sector-focused.

Healthcare M&A is no longer defined by aggressive expansion.

It is defined by precision, patience, and operational conviction.

VIII. Conclusion

Healthcare M&A in 2026 sits at a structural inflection point.

The survey data makes clear that the market’s primary constraint is no longer access to capital or availability of targets. It is confidence in execution. Integration risk, physician alignment, reimbursement stability, and technology integration now sit at the center of underwriting decisions.

At the same time, aggregate deal data tells a complementary story. Values are rebounding. Megadeals are returning. Regional capital flows are shifting. Strategic conviction — when present — is translating into scale.

This divergence defines the cycle.

The market is not broad-based and exuberant. It is concentrated and selective. Capital is flowing toward assets that offer:

Durable margins and recurring revenue

Clear regulatory pathways

Defensible innovation

Scalable data and AI capabilities

Realistic integration roadmaps

The era of rapid multiple expansion and leverage-driven returns has given way to a more operationally intensive model of value creation. Investors are underwriting productivity gains, technology-enabled efficiencies, and human capital retention. Operators are balancing growth with cultural and clinical stability. Cross-border innovation ecosystems are reshaping competitive dynamics.

And increasingly, M&A is serving as the primary catalyst for business model reinvention — accelerating the transition toward prevention-led, personalized, and digitally enabled care.

In this environment, winners will not simply transact. They will:

Structure capital creatively

Diligence operational complexity rigorously

Integrate technology systematically

Align physicians strategically

And deploy capital with conviction when resilience is demonstrable

Healthcare M&A is no longer defined by how many deals close.

It is defined by how well they perform after they do.

The next phase of value creation will belong to those who combine strategic focus with operational discipline — and who recognize that in this market, resilience is the new growth.

Sources and References:

Global M&A trends in health industries

What Will Matter Most for Successful Healthcare M&A in This Cycle?

What Will Really Slow Healthcare M&A in the Next 12 Months?

Where Healthcare M&A Is Most Likely to Hold Up in 2026