- Healthcare 150

- Posts

- Too Many MA Plans, Real AI Workflows, and a $1.11B Advisory Bet

Too Many MA Plans, Real AI Workflows, and a $1.11B Advisory Bet

Less noise in MA, more action in AI — and a $1B+ bet on advisory platforms.

Good morning, ! This week we are diving into the number of medicare advantage plans. autonomous ai agents now executing complex workflows, and Savills move into investment banking.

Want to advertise in Healthcare 150? Check out our ad platform, here.

Know someone in the healthcare space who should see this? Forward it their way. Here’s the link.

— The Healthcare150 Team

HEADLINE OF THE WEEK

AI Gets Autonomy — and Healthcare Gets a Reality Check

AI in healthcare has moved from experimentation to real-world deployment, with autonomous AI agents now executing complex workflows like claims processing and patient scheduling—driving efficiency gains and reducing administrative burden.

However, scaling AI introduces key challenges: interoperability and data fragmentation limit effectiveness, EHR vendors are consolidating control through embedded AI platforms, and governance is shifting toward continuous oversight rather than static frameworks. At the same time, security risks are rising as non-human identities accessing patient data multiply.

Bottom line: Agentic AI is transforming healthcare operations, but success depends on balancing innovation with strong data integration, governance, and security controls.

(More)

PRESENTED BY JUNIPER SQUARE

New fund formats call for a new operating model: fund operations partner.

Our report on the rise of new fund formats shows a clear shift: operating cadence is increasing, investor workflows are getting more complex, and expectations are moving toward to “always-on.”

That’s why leading PE firms are shifting to a fund operations partner model: one system of record + embedded expertise to run fundraising, investor operations, reporting, and administration with consistent data.

Juniper Square combines purpose-built software + expert fund administration services into a single connected operating model, delivering clearer visibility, fewer failure points, and a modern investor experience.

Read the full breakdown in the report.

Supporting our sponsors supports our free newsletters. Please support our sponsors!

DEAL OF THE WEEK

Savills Expands into Investment Banking with $1.11B Eastdil Acquisition

Savills’ acquisition of Eastdil Secured for $1.11B at 9.9x 2025 EBITDA is a direct bet on fee pools tied to large-scale asset transactions, not traditional brokerage. Eastdil’s $633M revenue and $113M EBITDA base is heavily skewed to North America at 76%, giving Savills immediate exposure to deeper capital markets and more complex deal structures.

The strategic shift is clear. This moves Savills up the value chain into advisory-led, high-margin services such as M&A, structured credit, and capital formation. It also creates a more resilient earnings mix less dependent on cyclical leasing volumes.

Why this matters for healthcare: healthcare real estate is increasingly institutional, capital-intensive, and transaction-driven. As hospitals, life sciences campuses, and outpatient networks consolidate, advisory firms with investment banking capabilities will capture disproportionate value. This deal signals where intermediaries are repositioning ahead of that shift.

The financing structure adds risk. A bridge facility of up to $800M at 5.5% to 6.0% introduces near-term refinancing pressure. But equity rollover of 16% and 6.3% insider ownership aligns incentives.

Bottom line: advisory is consolidating around capital markets expertise. Healthcare assets will follow. (More)

MICROSURVEY

What is currently the single biggest driver of cost increases in your organization? |

REGIONAL FOCUS

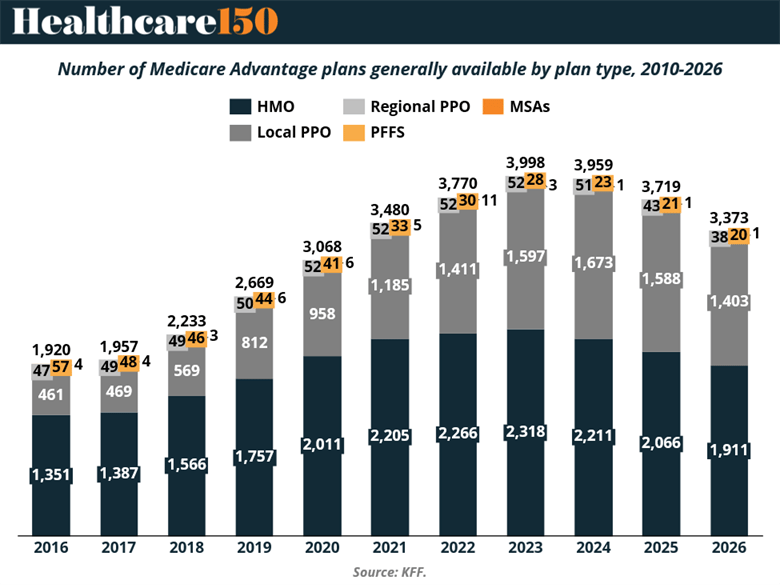

Medicare Advantage Plan Supply Contracts After 2023 Peak

After years of expansion, Medicare Advantage plan supply is finally cooling. Total plans peaked at 3,998 in 2023, before falling to 3,373 in 2026—a clear shift from growth to rationalization.

The biggest pullback? Local PPOs, which had been the industry’s favorite growth lever. HMOs, still the market’s backbone, are also trimming after their 2023 high.

Importantly, this isn’t about demand. Enrollment continues to rise—but insurers are cutting excess plan SKUs and doubling down on profitable geographies.

Blame the backdrop: tighter CMS rates, higher medical utilization, and more scrutiny on risk adjustment.

Bottom line: The land grab is over. Scale and margin discipline are now driving strategy. (More)

“It is health that is real wealth and not pieces of gold and silver.”

Mahatma Gandhi