- Healthcare 150

- Posts

- Medicare Advantage Plan Supply Contracts After 2023 Peak

Medicare Advantage Plan Supply Contracts After 2023 Peak

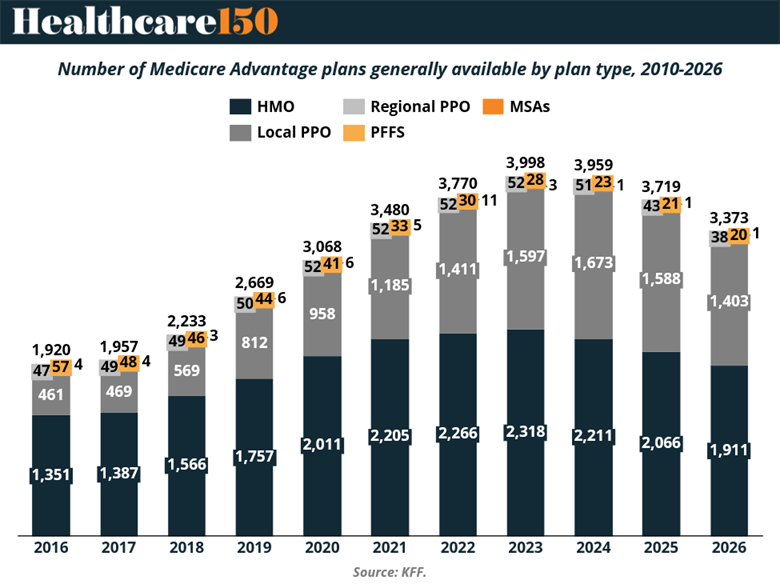

The total number of Medicare Advantage plans available nationwide declined again in 2026, continuing the retrenchment that began after the 2023 peak.

After expanding steadily from 1,920 plans in 2016 to a high of 3,998 plans in 2023, total plan count fell to 3,959 in 2024, 3,719 in 2025, and 3,373 in 2026. While supply remains materially higher than pre-2020 levels, the directional shift is clear: the expansion cycle has slowed, and insurers are reducing plan proliferation.

The pullback has been most visible in Local PPO offerings, which grew aggressively between 2018 and 2023 but have since declined meaningfully. HMO plans — the backbone of Medicare Advantage — also peaked in 2023 before contracting over the past two years. Regional PPO and Private Fee-for-Service (PFFS) plans remain small components of the overall market and have continued to decline in relative importance.

This shift suggests a period of portfolio rationalization rather than structural demand weakness. Enrollment in Medicare Advantage continues to grow, but insurers are concentrating offerings in markets where scale, network stability, and risk-adjusted economics are more predictable. In other words, the number of beneficiaries is increasing — the number of plan SKUs is not.

The divergence between enrollment growth and plan supply contraction indicates a maturing market. During the 2018–2023 expansion phase, insurers often introduced multiple plan variations within the same county to optimize pricing tiers and star positioning. The current environment, characterized by tighter CMS rate updates, elevated medical utilization, and heightened scrutiny of risk adjustment practices, appears to be encouraging consolidation rather than proliferation.

From a competitive standpoint, fewer total plans do not necessarily imply reduced competition. Instead, the data suggest that scale players are narrowing their focus while smaller or marginal offerings are being eliminated. This dynamic is consistent with broader signals across the Medicare Advantage landscape: growth remains intact, but capital efficiency and margin discipline are becoming more central to strategy.