- Healthcare 150

- Posts

- AI Meets Friction, Deals Pick Up, and Pharmacies Go Last-Mile

AI Meets Friction, Deals Pick Up, and Pharmacies Go Last-Mile

This week we’re diving into the AI in Healthcare Market, Consumer AI and data integration partnerships details, health industries deal volumes, and mobile pharmacy delivery competitive landscape.

Good morning, ! This week we’re diving into the AI in Healthcare Market, Consumer AI and data integration partnerships details, health industries deal volumes, and mobile pharmacy delivery competitive landscape.

Want to advertise in Healthcare 150? Check out our ad platform, here.

Know someone in the healthcare space who should see this? Forward it their way. Here’s the link.

— The Healthcare150 Team

DATA DIVE

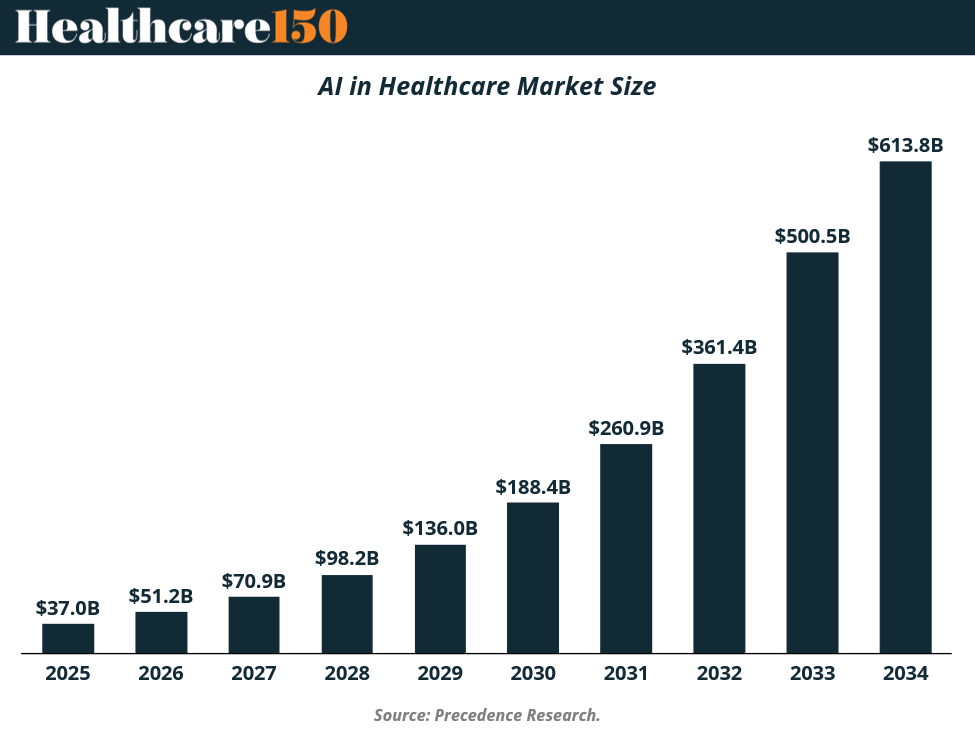

The $600B Inflection Point

AI in Healthcare is no longer a side project—it’s becoming core infrastructure. The market is projected to scale from $37B in 2025 to $613B by 2034, with the sharpest acceleration post-2030.

What’s driving it? Three forces: Data Explosion, Operational Pressure, and Maturing AI Capabilities. Health systems aren’t adopting AI for novelty—they’re doing it because they’re short on staff and long on costs. The shift is subtle but important: AI is moving from workflow optimization to clinical decision support.

Why it matters: This isn’t a single-vertical opportunity. AI is spreading horizontally across MedTech, pharma, and care delivery, turning into a platform layer.

The bottom line: Healthcare AI isn’t early anymore—it’s entering its scale phase, with the real value creation still ahead.

HEALTHTECH CORNER

AI Becomes the Interface, Not the Feature

Rock Health is retiring “AI deal” tracking altogether. Why? Because AI is now table stakes. Every serious digital health company is built with it, not around it. The implication is straightforward: AI alone no longer differentiates, workflow integration does.

At the same time, Q1 2026 marked a clear shift back to D2C healthcare, with new entrants like OpenAI and Perplexity launching consumer-facing health products. These platforms are emerging as front doors to care, aggregating data across EHRs, wearables, and diagnostics to deliver personalized insights.

This creates a new power dynamic. Consumer AI platforms gain longitudinal health data + user context; digital health players gain distribution. But it also introduces platform risk, echoing how iOS and Android became gatekeepers.

Why it matters: Healthcare is entering a phase where data aggregation + user ownership define value. The winners won’t be those with the best models—but those controlling the interface to the patient. (More)

COMPLIANCE CORNER

From Checklist to Control Tower: CMS Raises the Bar (Quietly)

CMS is enforcing it harder. The 2026 Conditions of Participation (CoPs) sharpen focus on clinical quality, infection control, and staffing sufficiency, with reimbursement increasingly tied to accurate coding and patient outcomes.

The shift is subtle but material: survey scrutiny is intensifying, and lapses, especially in infection protocols or readmission performance, are now directly linked to penalty risk. At the same time, site-neutral policies are pushing care into more cost-effective settings, raising the bar for documentation and decision-making.

Add in new requirements around pricing transparency (including algorithm-driven charges), and compliance is no longer siloed.

Bottom line: CoPs are evolving from a regulatory checklist into a real-time operating system for quality, reimbursement, and risk. (More)

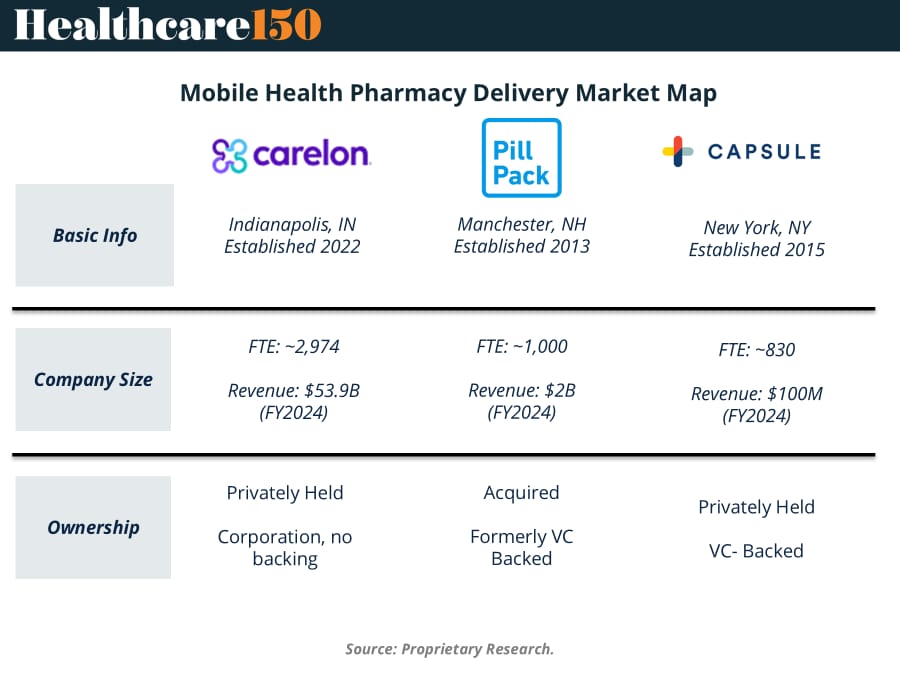

COMPETITIVE LANDSCAPE SNAPSHOT

TREND TO WATCH

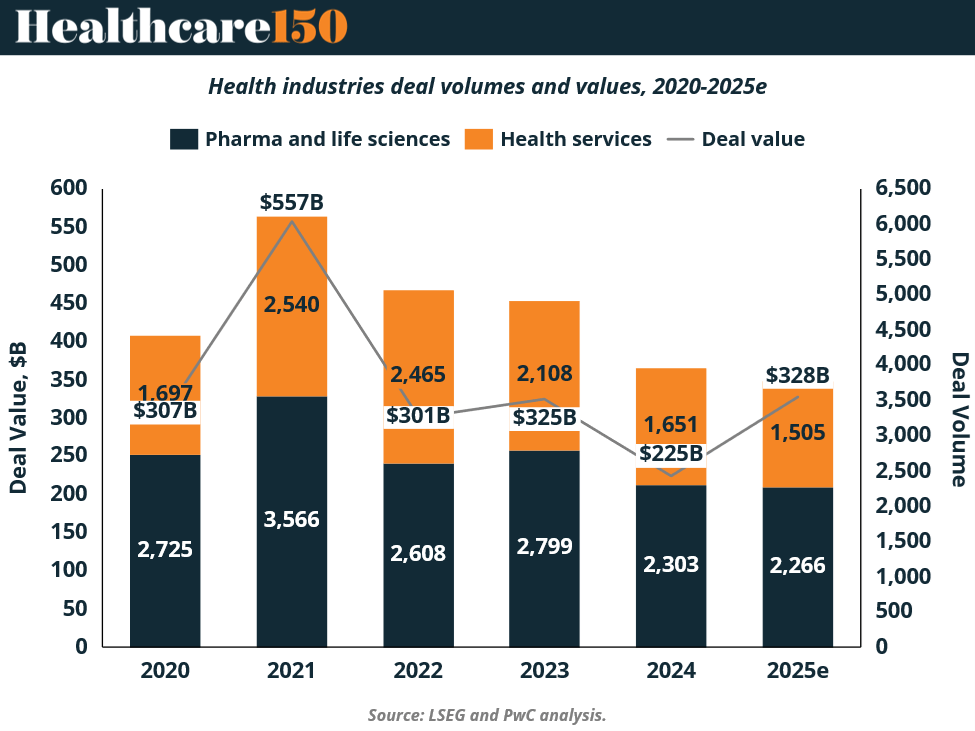

Fewer Deals, Bigger Checks

Healthcare M&A is quietly shifting gears. Deal Value jumped 46% in 2025, even as Deal Volume slipped 5%. The headline: scale is back.

Only 11 Megadeals ($5B+) closed—but that’s up from just three a year prior. Translation: fewer swings, but they’re landing harder.

The cycle tells the story. 2021 was peak liquidity. 2022–2024 was the hangover. 2025? A reset—$328B in value, driven by conviction, not volume.

Why it matters: Strategic buyers and sponsors aren’t chasing breadth—they’re underwriting platform assets and capability plays.

The bottom line: The market didn’t slow down, it got selective. And selective markets tend to reward the bold. (More)

"All progress takes place outside the comfort zone."

Michael John Bobak