- Healthcare 150

- Posts

- The Healthcare Transformation of the Wellness Economy and the Fitness Technology Ecosystem

The Healthcare Transformation of the Wellness Economy and the Fitness Technology Ecosystem

I. Introduction

The global wellness economy has transitioned from a discretionary consumer lifestyle segment into a structurally embedded extension of the healthcare industry. What was once categorized as elective self-care has evolved into a foundational component of preventive health infrastructure. In 2024, the global wellness economy reached approximately $6.8 trillion, expanding 7.9% year-over-year and more than doubling in size since 2013. This expansion is not merely cyclical recovery following the pandemic—it reflects a durable realignment of spending toward prevention, risk reduction, longevity, and quality-of-life optimization.

From a macroeconomic perspective, wellness has outpaced global GDP growth for over a decade, compounding at roughly 6.5% annually between 2013 and 2024 versus approximately 3.2% for global GDP. As of 2024, wellness represents more than 6% of total global economic output. Forward projections indicate sustained annual growth near 7.6% through 2029, bringing the total addressable market close to $9.8 trillion.

Within this broader healthcare-aligned transformation, fitness—and increasingly fitness technology—has emerged as a critical preventive health vertical. Fitness is no longer limited to recreational gym activity; it now functions as a distributed health monitoring and behavioral modification system supported by digital platforms, connected devices, biometric tracking, AI-enabled coaching, employer health programs, and outcomes-linked partnerships with payers and providers.

This report evaluates the wellness economy through a healthcare systems lens. It examines market size and growth, sector composition, the clinical relevance of physical activity, the digitization of behavioral health interventions, the modernization of fitness infrastructure, and M&A dynamics that illustrate capital concentration around measurable health outcomes.

II. The Wellness Economy

The wellness economy now operates as a multi-sector extension of the global healthcare ecosystem. Its $6.8 trillion scale in 2024 spans eleven interrelated sectors that collectively address prevention, chronic disease mitigation, mental health support, and quality-of-life enhancement.

At the top tier are three trillion-dollar segments:

Personal Care & Beauty ($1.35T)

Healthy Eating, Nutrition & Weight Loss ($1.148T)

Physical Activity ($1.144T)

These categories increasingly intersect with medical priorities such as obesity management, metabolic health, cardiovascular risk reduction, and aging-related conditions.

A second tier includes Wellness Tourism ($894B) and Public Health, Prevention & Personalized Medicine ($676B), both of which are increasingly integrated into healthcare-adjacent service models. A third tier—Traditional & Complementary Medicine ($606B) and Wellness Real Estate ($548B)—reflects the institutionalization of health-supportive environments. Finally, specialized services such as Mental Wellness ($268B), Spas ($157B), Springs ($72B), and Workplace Wellness ($53B) complete the sector landscape.

This composition is strategically significant for healthcare stakeholders. Physical activity alone represents a $1.144 trillion market, positioning it as a central pillar of preventive health strategy rather than a discretionary consumer category. Moreover, physical activity drives downstream demand for diagnostics, wearable monitoring, nutrition therapeutics, recovery modalities, and mental health tools—blurring traditional boundaries between lifestyle and clinical care.

From a macro comparison standpoint, the wellness economy now exceeds multiple globally recognized industries. At $6.8T in 2024, it surpasses IT ($5.3T), tourism ($5.1T), the green economy ($5.1T), sports ($2.7T), and even pharmaceutical revenues (~$1.8T). Only total healthcare expenditures (~$11.2T) and manufacturing (~$16.8T) remain larger in aggregate scale.

This comparison reinforces a structural conclusion: wellness is no longer an ancillary consumer trend—it is a major global healthcare-aligned spending complex.

The trajectory since 2019 further illustrates resilience. After a temporary contraction from $5.0T (2019) to $4.7T (2020), the market rebounded rapidly and reached $6.8T by 2024. Projections indicate continued growth to approximately $9.8T by 2029.

Regionally, North America, Europe, and Middle East–North Africa have demonstrated particularly strong post-pandemic recovery. Importantly, all eleven sectors have exceeded their 2019 levels by 2024. Two sectors—Wellness Real Estate (19.5% CAGR) and Mental Wellness (12.4% CAGR)—have expanded at structurally elevated rates, indicating that health-supportive environments and psychological well-being are becoming embedded into built infrastructure and daily life systems.

Operationally, the wellness economy is shifting toward outcome measurement, personalization, and continuous monitoring—key attributes historically associated with healthcare delivery models. Consumers now expect biometric feedback, adaptive programming, and quantified progress. This evolution directly sets the stage for the healthcare convergence of the fitness technology vertical.

III. The Fitness Technology Ecosystem as Preventive Healthcare Infrastructure

Fitness technology now operates at the intersection of physical activity and digital health infrastructure. The category includes wearable biometrics, connected equipment, virtual coaching, AI-driven personalization engines, corporate wellness platforms, and data integration layers that increasingly connect with insurers and providers.

The strategic healthcare implication is clear: physical activity is a core determinant of chronic disease risk, yet adherence remains historically low. Technology enables scalable behavior modification, monitoring, and engagement—turning episodic exercise into a measurable health intervention.

Smart Fitness: The Consumer Health Operating System

The global smart fitness market is projected to reach $71.9B in 2025 and expand to $186.1B by 2034, reflecting an approximately 11.15% CAGR.

Wearables currently anchor the category by serving as the primary biometric capture layer (heart rate variability, activity levels, sleep metrics, recovery indicators). However, the fastest-growing segments include immersive connected equipment and AI-enhanced training ecosystems.

The structural shift is from passive tracking to active health optimization. Hardware remains a significant revenue contributor, but software platforms and subscription services are the fastest-growing segment—mirroring broader healthcare digitization trends.

In the United States, the smart fitness market is projected to expand from $20.1B (2025) to $53.1B (2034), demonstrating continued monetization even in mature markets.

Strategic risks include data privacy concerns and regulatory exposure as devices increasingly integrate with healthcare systems. Competitive commoditization of hardware further emphasizes the need for proprietary data, validated outcomes, and ecosystem stickiness.

Online and Virtual Fitness: Scalable Behavioral Intervention

Online and virtual fitness represents one of the fastest-growing subsegments. The market is projected to grow from $38.4B (2025) to $138.7B (2030), reflecting an approximate 29% CAGR.

Growth drivers now extend beyond convenience. AI-enabled adaptive programming, wearable integration, and senior population adoption support sustained expansion. Importantly, virtual fitness reduces barriers to participation and enables remote monitoring—aligning with telehealth models and distributed care delivery.

Revenue models are evolving toward subscription-based ecosystems, hybrid monetization, and enterprise contracts across corporate, educational, and institutional channels.

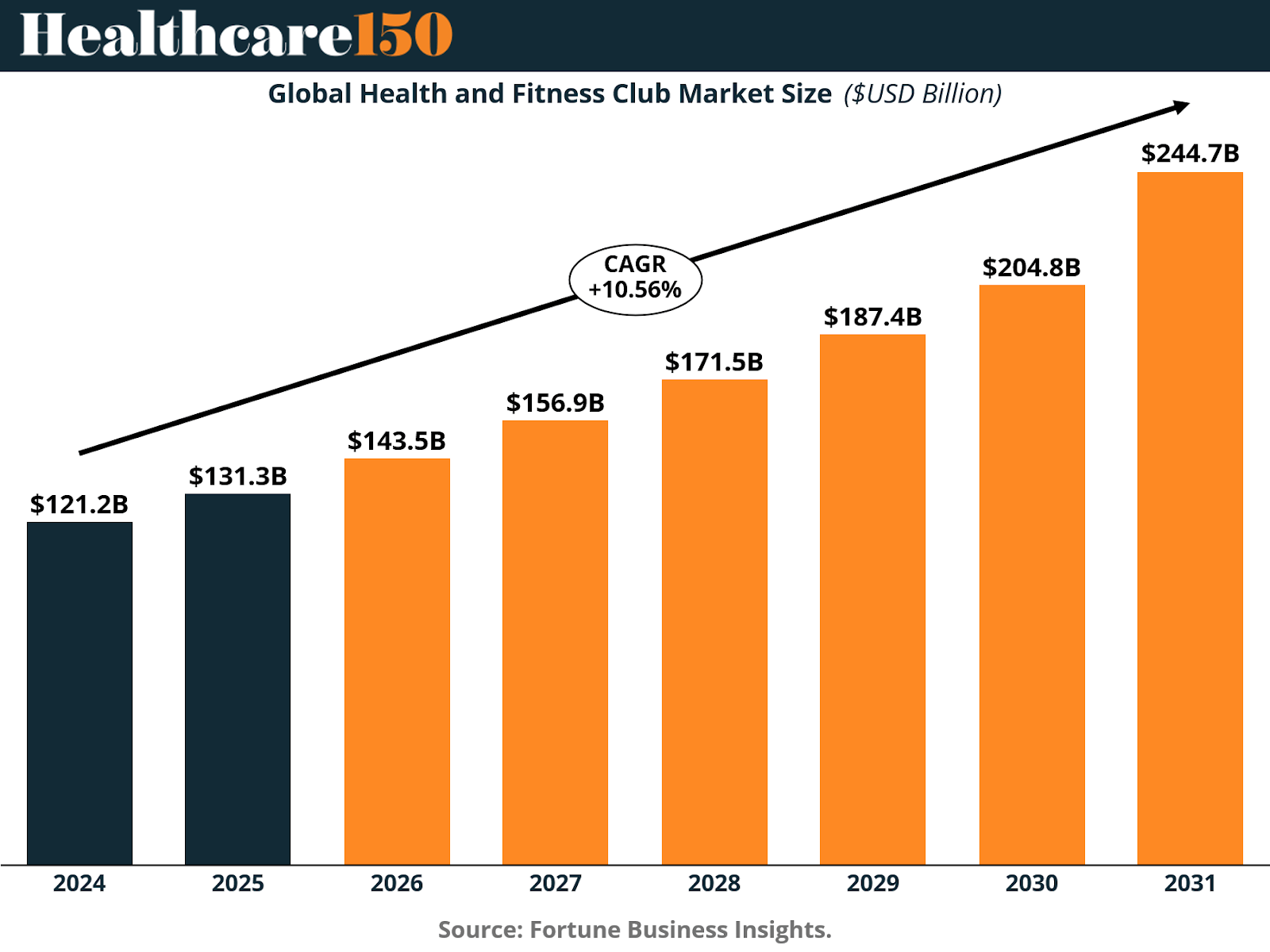

Fitness Clubs: Hybrid Healthcare-Enabled Physical Infrastructure

The global health and fitness club market is projected to grow from $121.2B (2024) to $244.7B (2031).

Personal training represents approximately 47% of revenue by service mix, indicating growing demand for expert-guided outcomes. Self-training accounts for roughly 35%, and group training approximately 18%.

North America demonstrates a particularly strong recovery trajectory, projected to approach $106.0B by 2032.

Modern clubs increasingly function as hybrid healthcare venues, integrating recovery zones, metabolic testing, and digital engagement layers. However, high fixed costs and competition from home-based alternatives require clubs to articulate differentiated hybrid value propositions.

The emerging model is not gym versus home, but integrated health continuity across environments.

Structural Drivers

Key forces shaping the vertical include:

Rising chronic disease burden driving preventive urgency

AI-enabled personalization at scale

Hybrid delivery models

Subscription-based platform economics

Corporate healthcare cost containment

Immersive and gamified engagement models

Integration with healthcare systems for measurable outcomes

The unifying theme is the transformation of fitness into measurable, data-integrated preventive healthcare.

IV. M&A and Deal Landscape

M&A activity reflects consolidation around scalable, data-driven healthcare-aligned platforms. Deal value reached $114.8B in 2017, normalized through 2019, re-accelerated in 2020–2022, adjusted in 2023–2024, and rebounded to $77.2B in 2025.

The pattern suggests investor appetite for integrated ecosystems that combine biometric capture, AI-driven personalization, content distribution, and physical infrastructure.

Strategic buyers increasingly pursue assets that strengthen outcome validation, improve retention, and expand enterprise partnerships. The premium accrues to businesses controlling the user relationship and demonstrably improving measurable health metrics.

V. Conclusion

The wellness economy has evolved into a healthcare-adjacent macro system of global significance. At $6.8 trillion in 2024, with projections approaching $9.8 trillion by 2029, it represents one of the largest and fastest-growing structural spending complexes worldwide.

Fitness sits at the center of this transformation. Clubs are modernizing, virtual platforms are scaling rapidly, and smart fitness technologies are building the digital backbone of preventive health monitoring. The strategic convergence is clear: wellness is integrating into healthcare, and fitness is becoming a measurable, personalized intervention layer within that system.

The next decade will be defined not by isolated devices or facilities, but by end-to-end ecosystems capable of delivering validated outcomes across home, workplace, and clinical environments.

For operators, investors, and healthcare stakeholders, the opportunity lies in owning the personalization layer, proving health impact, and embedding fitness into formal preventive care pathways. The long-term winners will be those that translate biometric data into sustained behavioral change—and measurable improvements in population health at scale.

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|

Want to check the other reports? Access the Report Repository here.