- Healthcare 150

- Posts

- The Cost Squeeze: Why Healthcare Economics Break in 2025

The Cost Squeeze: Why Healthcare Economics Break in 2025

Healthcare cost inflation is no longer a single-variable problem. It is a system-wide compression cycle where premiums, labor, reimbursement, and consumer affordability are all moving in conflicting directions.

The result is not just rising costs. It is a structural imbalance that the system cannot easily absorb.

Premiums continue their steady climb, but affordability is deteriorating faster than pricing power can compensate. At the same time, provider cost bases, led overwhelmingly by labor at $890B, are expanding far beyond what reimbursement mechanisms, particularly Medicare’s 5.1% IPPS increase, can sustain against 14.1% inflation. This creates a widening gap that no single stakeholder can close.

What emerges heading into 2025 is a system under synchronized pressure. Patients are more price-sensitive, providers are margin-constrained, and payers face growing resistance to further premium increases. The implication is clear. Healthcare is not just becoming more expensive. It is becoming economically unstable.

The Cost Curve That Never Broke

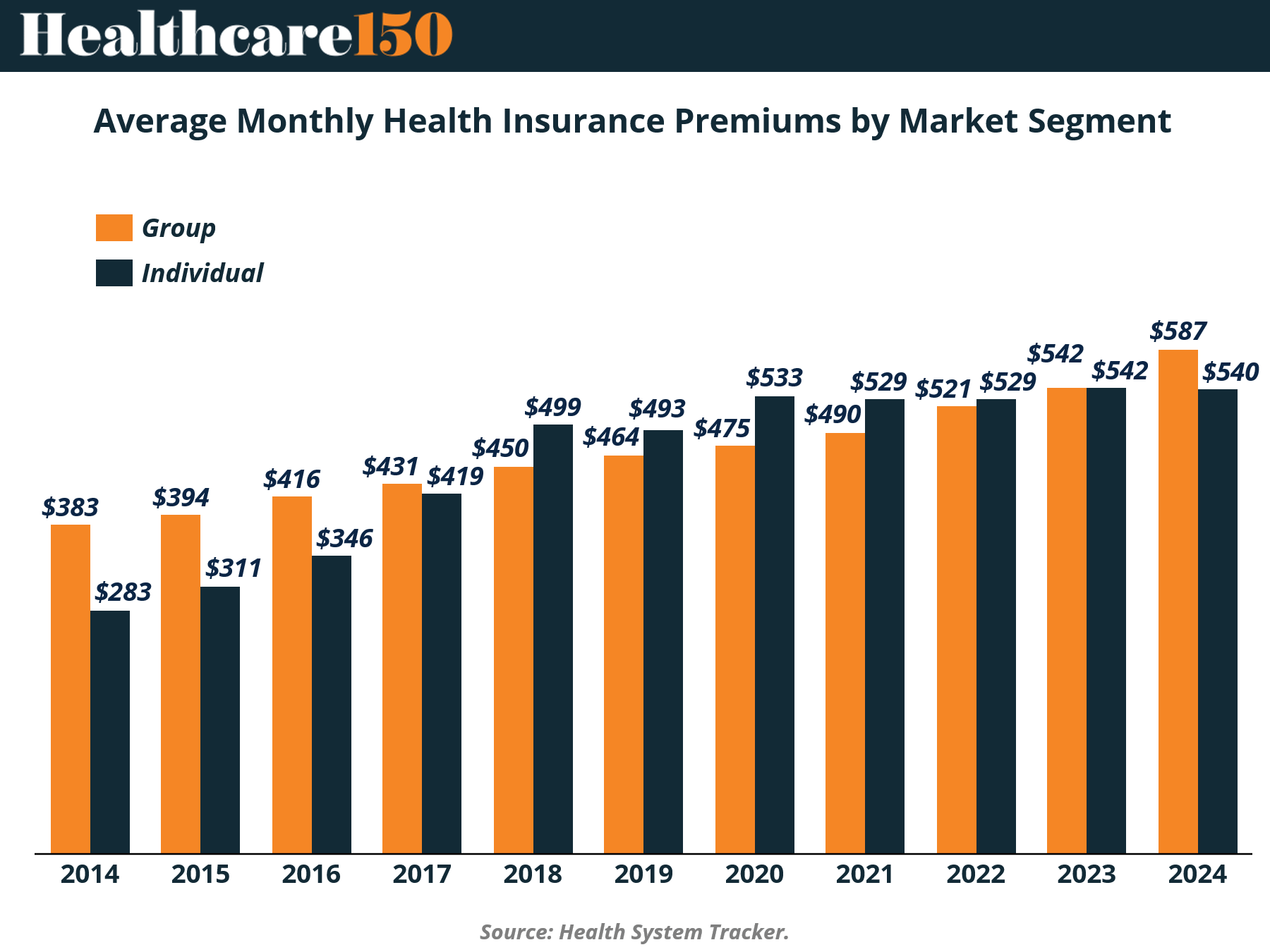

Health insurance premiums did not spike in 2025. They compounded. Over the past decade, average monthly premiums climbed from $383 to $587 in the group market and from $283 to $540 in the individual market. That is not volatility. That is structural inflation embedded into the system.

What stands out is not just the upward trajectory, but the convergence. Individual premiums, once meaningfully lower, have nearly closed the gap with employer-sponsored plans. By 2023, both segments sat at $542, signaling a shift in risk pooling dynamics. The individual market is no longer a discounted alternative. It is pricing closer to true cost, with fewer buffers.

The implication heading into 2025 is clear. Cost pressure is no longer isolated to employers or subsidized populations. It is system-wide and synchronized. As premiums approach parity across segments, differentiation shifts away from pricing and toward network design, utilization control, and risk selection. The era of segment-driven pricing advantage is fading.

Key Bulleted Analysis

Premium growth from 2014 to 2024 shows a steady CAGR, not episodic spikes, indicating persistent cost drivers, not cyclical ones

Convergence at ~$540+ suggests risk pools are normalizing, reducing arbitrage between group and individual markets

Employers lose historical pricing advantage, increasing pressure on self-insurance and alternative benefit design

Individual market affordability becomes structurally strained as premiums approach employer levels without equivalent subsidies

For payers, margin expansion will depend less on premium growth and more on medical cost management and underwriting precision

For investors, signals favor cost-containment infrastructure, including RCM, utilization analytics, and care navigation platforms

Affordability Anxiety Is No Longer Healthcare-Specific

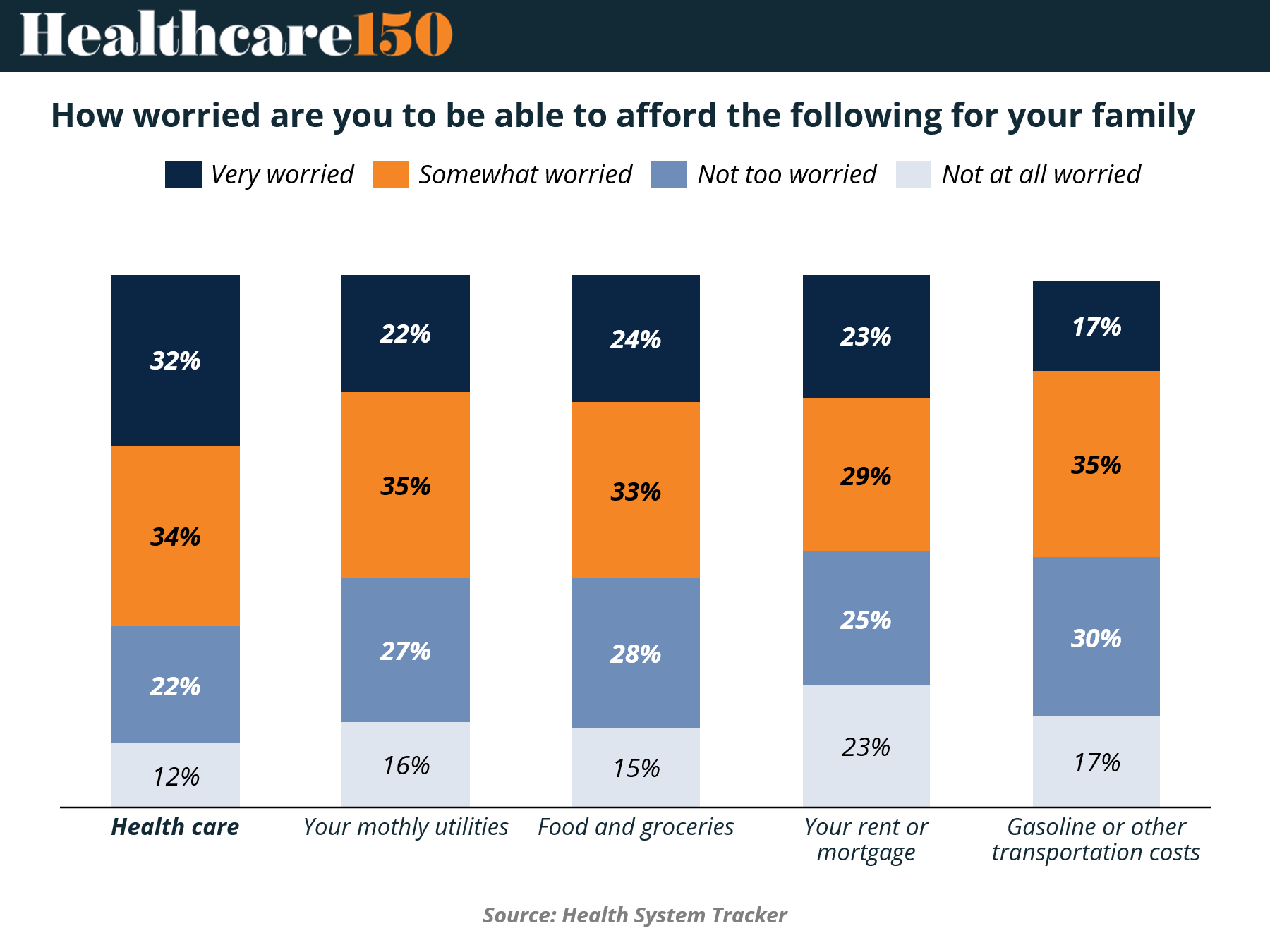

Healthcare costs remain the single largest source of financial anxiety, but the more important signal is comparative. 66% of respondents report being either very or somewhat worried about affording healthcare, higher than any other category measured. That leadership position matters. It confirms that healthcare is not just expensive. It is perceived as unpredictably expensive.

But the gap is narrowing. Essentials like utilities (57% worried), food (57%), housing (52%), and transportation (52%) are converging toward healthcare in perceived financial strain. This is a critical shift. Healthcare is no longer an outlier. It is competing for wallet share in an environment where all core expenses are under pressure.

For 2025, this reframes the affordability debate. The issue is no longer whether patients can afford healthcare in isolation. It is whether they can afford healthcare relative to everything else. That distinction drives behavior. Delayed care, plan downgrades, and utilization deferral are no longer edge cases. They become rational economic decisions in a constrained household budget.

Key Takeaways

The 66% concern level in healthcare signals persistent pricing opacity and volatility, not just high absolute cost. Investors should view this as a demand elasticity risk, not a pricing strength

Convergence across categories suggests macro pressure is now healthcare’s primary demand driver, reducing the sector’s historical insulation from economic cycles

Rising concern in non-health categories compresses discretionary healthcare spend first, particularly in elective procedures, specialty pharmacy adherence, and preventative care utilization

Expect increased bad debt and collection pressure for providers as households triage expenses, particularly in high-deductible plan populations

Payers face a structural tension. Premium growth may be necessary, but affordability ceilings are becoming more visible and politically sensitive

Medicaid and subsidized exchange enrollment may rise as affordability thresholds are breached, creating payer mix shifts with lower margins for providers

Employers are likely to accelerate cost-shifting strategies such as higher deductibles and narrower networks, further reinforcing consumer sensitivity to out-of-pocket exposure

This environment favors low-cost care delivery models including outpatient migration, virtual-first care, and value-based primary care platforms

Pharma faces second-order risk through adherence erosion, particularly for chronic therapies where cost-sharing drives abandonment

For investors, the signal is clear. Growth will concentrate in models that reduce perceived and actual out-of-pocket burden, not those that rely on continued pricing power

Policy risk increases as affordability anxiety broadens beyond healthcare, raising the probability of rate scrutiny, subsidy expansion, or pricing intervention

Bottom line: Healthcare affordability is no longer a sector-specific issue. It is part of a broader household liquidity crisis, and that shift will redefine demand, utilization, and pricing power heading into 2025.

Fragmentation, Not Monopoly, Is Driving Market Power

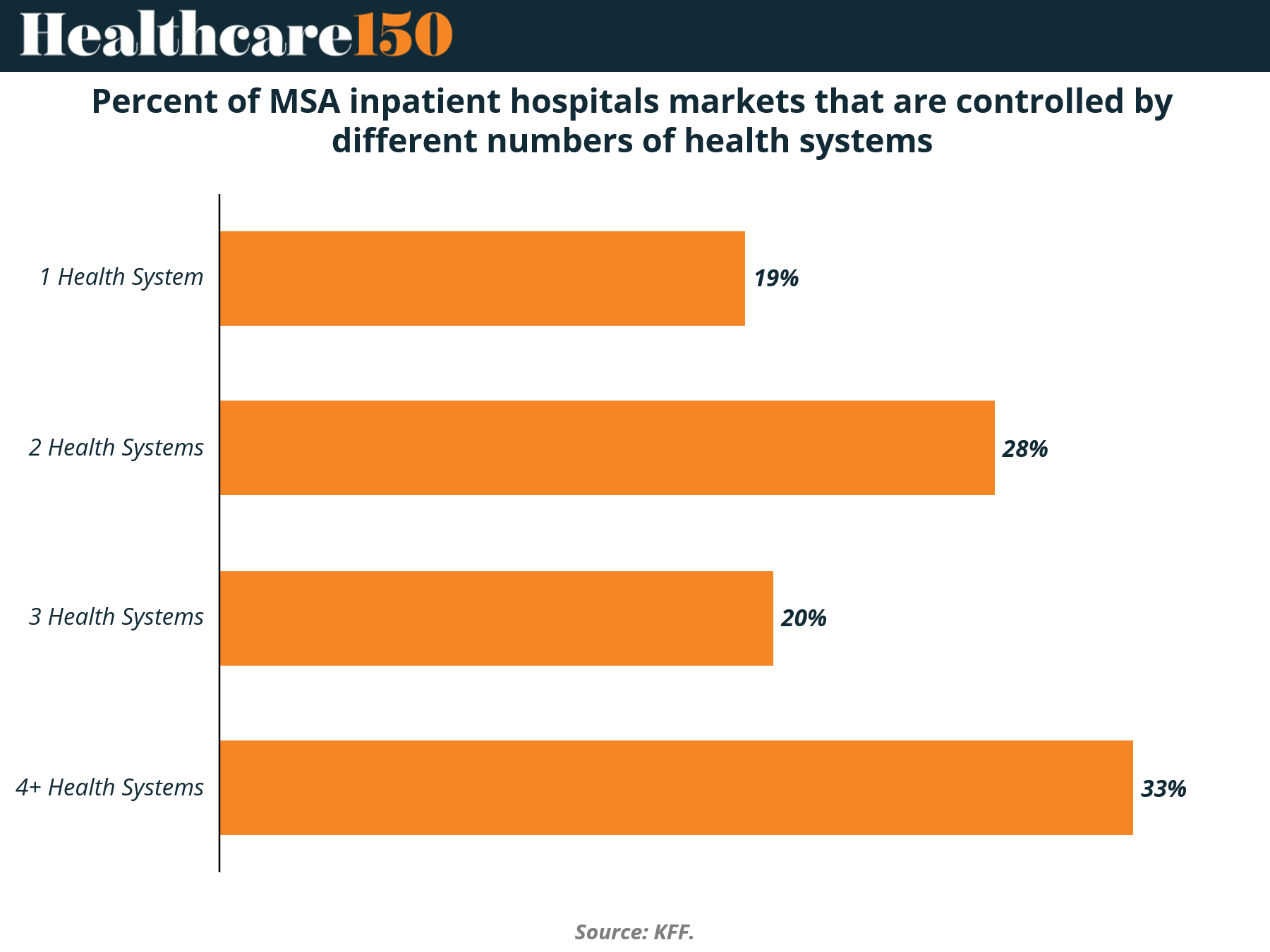

Hospital market concentration is often framed as a consolidation story. The data suggests something more nuanced. Only 19% of MSAs are controlled by a single health system, while the majority operate in multi-system environments, including 28% with two systems and 33% with four or more.

This is not a winner-take-all market. It is a fragmented oligopoly. Even in highly consolidated regions, competition persists, but it is concentrated among a small number of scaled players. That distinction matters. Pricing power does not require monopoly control. It requires limited, rational competition among large systems with similar cost structures.

Heading into 2025, this structure helps explain why cost inflation has proven so durable. Fragmentation at the national level masks local concentration effects. In many MSAs, a handful of systems effectively set pricing benchmarks, while smaller players lack the leverage to disrupt rate dynamics.

Key takeaways

With only 19% of markets controlled by a single system, regulatory focus on monopoly power may be misaligned with how pricing power actually manifests, which is through oligopolistic structures

The 28% of markets with two systems represent the highest-risk segment for pricing coordination dynamics, where competition exists but is structurally limited

The 33% share of markets with 4+ systems does not imply fragmentation in practice, as these markets are often dominated by a few large systems alongside smaller, non-scaling competitors

Scale remains the defining advantage. Larger systems negotiate more favorable rates with payers, reinforcing price elevation rather than price competition

For payers, fragmented provider landscapes increase contracting complexity and reduce leverage, particularly in must-have hospital systems

For employers, local market structure increasingly determines cost exposure more than national trends, reinforcing the need for market-specific benefit strategies

Private equity and strategics should view fragmented MSAs as roll-up opportunities, particularly in outpatient and adjacent services where hospitals are less dominant

Continued consolidation is likely, but future deals will face heightened antitrust scrutiny, slowing large-scale hospital M&A while shifting focus to vertical integration

Expect growth in non-hospital care delivery models as a competitive response, including ambulatory networks, home-based care, and value-based physician groups

Pricing pressure will persist not because markets are fully consolidated, but because they are consolidated enough to sustain elevated rates without triggering regulatory breakups

Bottom line: The hospital market is not dominated by monopolies. It is structured for sustained pricing power through concentrated competition, a dynamic that will continue to underpin healthcare cost inflation into 2025.

Labor Is the Cost Problem. Everything Else Is Noise

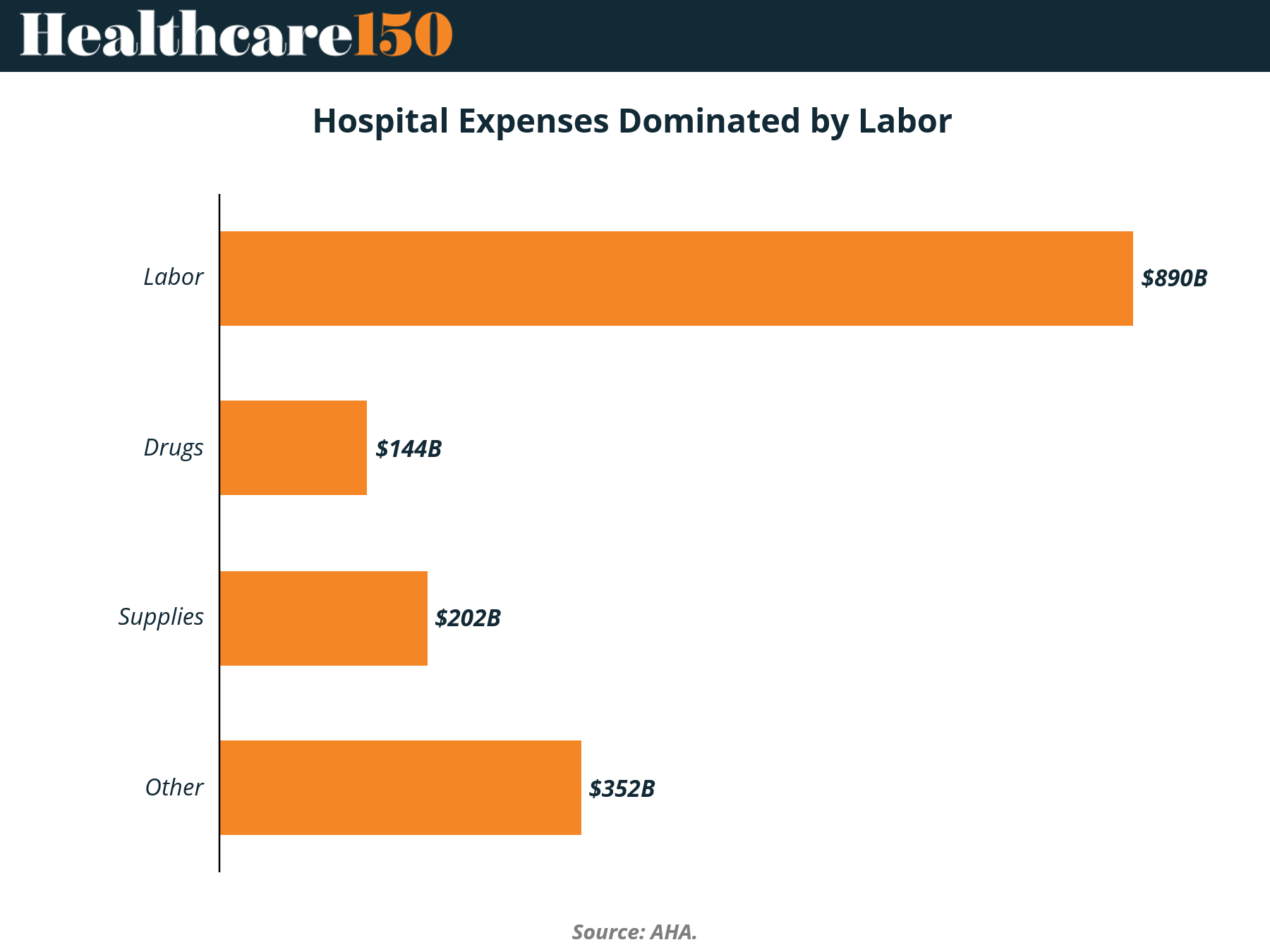

Hospital cost structures are often discussed as a mix of drugs, supplies, and administrative overhead. The data tells a simpler story. Labor alone accounts for $890B in expenses, more than double the combined spend on drugs ($144B) and supplies ($202B).

This is not just a large category. It is the category. Labor dominates hospital P&Ls to such an extent that marginal gains elsewhere have limited impact on overall cost trajectories. Efforts to negotiate drug pricing or optimize supply chains matter, but they operate at the edges of the cost base.

For 2025, this reframes the cost containment playbook. Healthcare inflation is fundamentally tied to workforce dynamics, including wage growth, staffing shortages, and productivity constraints. As long as labor remains structurally tight, cost compression will remain elusive regardless of progress in other categories.

Key Takeaways

Labor at $890B represents the primary driver of hospital cost inflation, making workforce economics the central variable for margin performance

Wage pressure is unlikely to normalize quickly given persistent clinical labor shortages, particularly in nursing and specialized roles

Reliance on contract labor during peak periods has structurally reset baseline costs higher, even as utilization of travel staff declines

Automation and AI adoption face a structural ceiling. Most hospital labor is clinical and cannot be easily replaced, limiting true cost-out potential from technology

Productivity gains, not headcount reduction, will define successful operators, shifting focus toward workflow optimization, staffing models, and care standardization

Smaller and rural hospitals face disproportionate pressure, as they lack scale to absorb rising labor costs, increasing risk of closures or consolidation

For payers, sustained provider cost inflation reinforces premium increases and reimbursement tension, particularly in commercial markets

Pharma and supply-side cost controls will have limited system-wide impact unless labor inflation is addressed in parallel

Investors should prioritize models that decouple care delivery from traditional labor intensity, including home-based care, tech-enabled services, and task-shifting platforms

Long-term, the system may see a reconfiguration of care delivery roles, with mid-level providers and digital augmentation absorbing portions of physician and nurse workload

Policy risk is rising as labor costs translate directly into affordability challenges, increasing the likelihood of rate regulation or workforce subsidies

Bottom line: Healthcare cost inflation is not a drug pricing problem or a supply chain problem. It is a labor problem, and until that changes, margin pressure across the system will persist into 2025 and beyond.

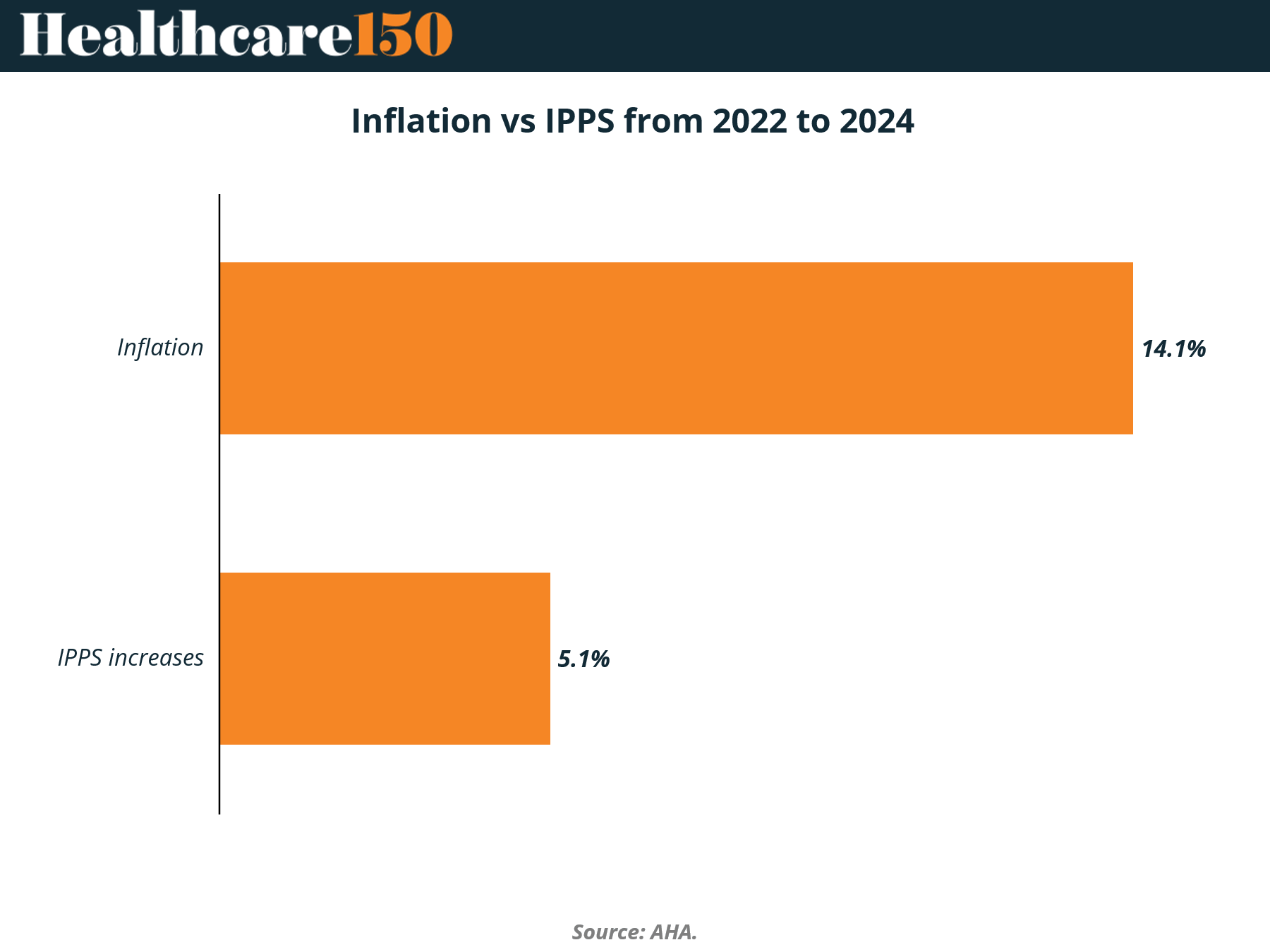

Reimbursement Is Not Keeping Up. The Gap Is Structural

Between 2022 and 2024, hospital cost inflation rose 14.1%, while Medicare inpatient reimbursement through IPPS increased just 5.1%. That delta is not a temporary mismatch. It is a structural gap between cost growth and payment updates.

This divergence is where margin compression becomes inevitable. Hospitals cannot reprice Medicare patients, and public payers already represent a significant share of volume. When reimbursement fails to track cost inflation, the shortfall does not disappear. It shifts. Typically into commercial pricing, cost-cutting, or service reductions.

Heading into 2025, the implication is clear. The system is entering a period where reimbursement lag becomes the primary constraint on financial performance. Unlike labor or supply costs, this is not an operational variable. It is policy-driven and slow to adjust, creating sustained pressure across providers.

Key Takeaways

The ~9 percentage point gap between inflation (14.1%) and IPPS updates (5.1%) represents a direct margin compression driver, particularly for Medicare-heavy providers

Hospitals with higher public payer mix will face disproportionate financial strain, accelerating divergence between strong and weak operators

Cost shifting to commercial payers will intensify, reinforcing premium inflation and employer burden, but with increasing resistance from payers

Payers are likely to push back harder on rate increases, creating contracting friction and narrower networks as leverage tools

Persistent under-reimbursement may force hospitals to cut service lines, particularly low-margin or rural offerings, impacting access

Capital investment will slow, especially in infrastructure and innovation, as systems prioritize short-term margin preservation over long-term growth

This environment favors asset-light and outpatient models that are less exposed to fixed reimbursement structures and inpatient cost bases

Credit quality across not-for-profit health systems may deteriorate, increasing distress, refinancing risk, and potential consolidation opportunities

Policy intervention risk rises as hospital financial stress becomes more visible, but timing remains uncertain and unlikely to close the gap quickly

For investors, the key signal is clear. Returns will concentrate in models less dependent on regulated reimbursement and more aligned with cost control or alternative payment structures

Bottom line: The reimbursement gap is not cyclical. It is structural, and it will be one of the defining constraints on healthcare economics in 2025.

Conclusion

The throughline across every data point is not growth. It is constraint. Costs are rising in ways that are persistent, interconnected, and increasingly resistant to traditional levers like pricing, scale, or incremental efficiency gains.

For providers, the challenge is structural margin compression driven by labor intensity and reimbursement lag. For payers, it is the growing ceiling on premium increases as affordability deteriorates. For patients, it is a shift toward economic trade-offs that directly impact utilization and outcomes. No part of the system is insulated anymore.

For investors and operators, 2025 becomes a filter year. Models that depend on pricing power, inpatient volume, or reimbursement stability will face pressure. In contrast, models that reduce cost intensity, improve productivity, or align with value-based economics will capture disproportionate upside.

The healthcare system is not breaking all at once. It is tightening. And the winners will be those positioned to operate inside that constraint, not those betting it disappears.

Sources & References

Health System Tracker. Trends shaping 2026 costs. https://www.healthsystemtracker.org/chart-collection/eight-trends-shaping-2026-healthcare-costs/#Distribution%20of%20payer-specific%20negotiated%20rates%20for%20MRI%20of%20the%20lower%20spine,%20across%20ten%20hospitals,%202021

AHA. Cost caring report. https://www.aha.org/guides-and-reports/2026-03-09-2025-cost-caring-report

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|

Want to check the other reports? Access the Report Repository here.