- Healthcare 150

- Posts

- Sports Medicine Market: Growth, Innovation, and Investment Opportunities

Sports Medicine Market: Growth, Innovation, and Investment Opportunities

A deep dive into market expansion, regional dynamics, application trends, and the evolving competitive ecosystem shaping the future of musculoskeletal care

I. Introduction

The global sports medicine market is entering a new phase of accelerated growth, driven by the convergence of rising injury rates, aging yet increasingly active populations, and the continued professionalization of sports across all levels. What was once a niche segment primarily focused on elite athletes has evolved into a broad, multi-billion-dollar ecosystem, spanning orthopedic devices, surgical procedures, rehabilitation services, biologics, and performance optimization technologies.

Today, demand is being fueled not only by professional leagues, but also by a rapidly expanding base of recreational athletes, fitness-conscious consumers, and older populations seeking to extend mobility, independence, and overall quality of life. Increased participation in organized sports, the global rise of fitness culture, and greater awareness of musculoskeletal health are contributing to a steady increase in injury incidence—further reinforcing the need for effective, scalable treatment solutions.

At the same time, innovation is reshaping the landscape. Advances in minimally invasive procedures, regenerative medicine, and data-driven recovery protocols are improving clinical outcomes while reducing recovery times and overall healthcare costs. The integration of wearables, AI-powered diagnostics, and personalized rehabilitation programs is also transforming how injuries are prevented, monitored, and managed—expanding the scope of sports medicine beyond treatment into proactive and continuous care.

For investors and operators, sports medicine sits at a compelling intersection of healthcare delivery, consumer wellness, and innovation-led growth. The market remains highly fragmented, with a diverse mix of device manufacturers, outpatient clinics, therapy providers, and digital health platforms. This fragmentation, combined with strong underlying demand and favorable demographic tailwinds, creates significant opportunities for consolidation, platform building, and operational scale.

Looking ahead, the evolution of sports medicine will be shaped by both clinical innovation and shifting patient expectations, as individuals increasingly demand faster recovery, better outcomes, and more personalized care pathways. As a result, the market is poised not only for continued expansion, but for structural transformation in how musculoskeletal health is delivered and managed.

This report explores the key drivers, competitive dynamics, and investment opportunities shaping the future of the sports medicine market.

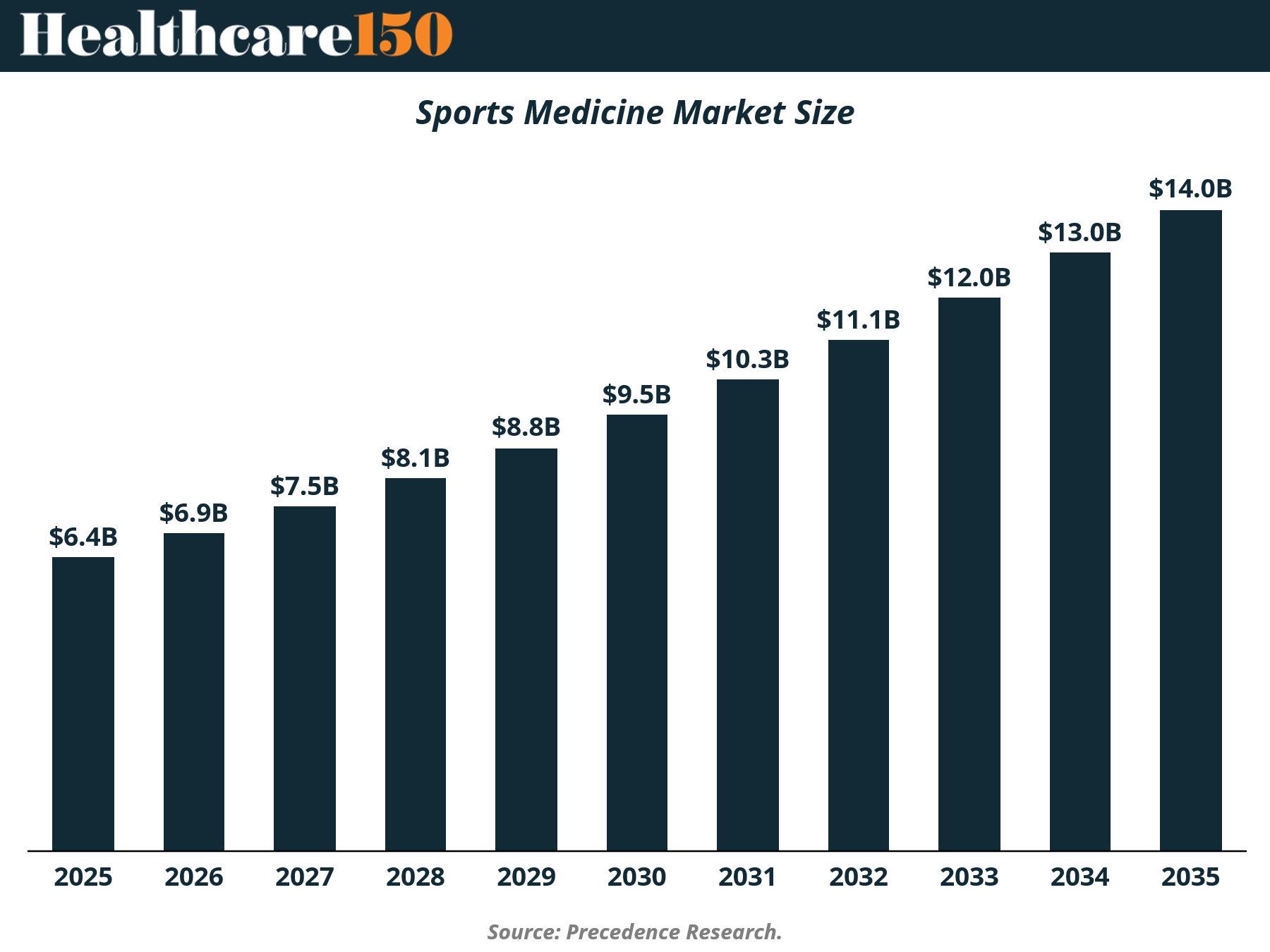

II. Sports Medicine Market Size

The global sports medicine market is demonstrating steady and resilient expansion, underpinned by strong structural demand and favorable long-term tailwinds. The market was valued at approximately $6.4 billion in 2025 and is projected to reach nearly $14.0 billion by 2035, representing a compound annual growth rate (CAGR) of 8.1% over the forecast period.

This growth trajectory reflects a consistent increase in demand across both treatment and prevention pathways, driven by rising participation in sports and physical activity worldwide. As fitness becomes more embedded in daily lifestyles, injury incidence is expected to rise in parallel—supporting sustained utilization of sports medicine products and services.

Importantly, the market’s expansion is not solely volume-driven. The increasing adoption of advanced surgical techniques, higher-value orthopedic devices, and specialized rehabilitation protocols is contributing to higher spend per patient, further accelerating revenue growth. In addition, the shift toward outpatient care settings and minimally invasive procedures is improving accessibility, enabling broader patient reach.

From a segmentation perspective, growth is expected to be supported by:

Orthopedic devices and implants, driven by innovation and procedural volume

Rehabilitation and physiotherapy services, benefiting from post-surgical demand and chronic injury management

Regenerative medicine and biologics, an emerging high-growth segment

Geographically, North America continues to dominate the market, supported by advanced healthcare infrastructure and high sports participation rates, while Europe and Asia-Pacific are expected to contribute meaningfully to future growth as access to care expands and awareness increases.

Overall, the sports medicine market presents a compelling mid-to-high growth profile, combining predictable demand drivers with innovation-led upside—positioning it as an attractive segment within the broader healthcare landscape.

III. Sports Medicine Regional Landscape

The global sports medicine market exhibits a highly uneven regional distribution, with growth concentrated in developed healthcare systems while emerging markets continue to gain momentum.

North America leads the market, accounting for approximately 47% of global share in 2025, driven by a combination of high sports participation rates, advanced healthcare infrastructure, and strong adoption of innovative treatment technologies. The region also benefits from significant spending power, widespread availability of specialized care, and a well-established ecosystem of orthopedic device manufacturers, rehabilitation providers, and sports performance centers. In addition, the presence of major professional sports leagues and a large base of recreational athletes continues to sustain demand.

Europe represents the second-largest market, holding around 23% share, supported by robust public healthcare systems and growing investment in sports science and injury prevention. Increasing awareness of musculoskeletal health, combined with aging populations that remain physically active, is driving steady demand across both surgical and non-surgical treatments.

The Asia-Pacific region, with approximately 16% market share, is emerging as a key growth engine. Rising disposable incomes, expanding access to healthcare, and increasing participation in organized sports are contributing to market expansion. Countries such as China, India, and Japan are seeing rapid development in healthcare infrastructure and sports medicine capabilities, positioning the region for accelerated growth over the coming decade.

Latin America and the Middle East & Africa currently account for smaller shares—approximately 9% and 6%, respectively—but present significant long-term upside. Growth in these regions is being supported by improving healthcare access, government investment, and a gradual increase in sports participation. However, market development remains constrained by limited infrastructure, lower healthcare spending, and uneven access to specialized care.

Overall, while developed markets continue to dominate in terms of revenue, emerging regions are expected to outpace in growth, driven by expanding access, demographic shifts, and increasing investment in healthcare systems. This dynamic creates opportunities for both market expansion and strategic geographic diversification for operators and investors alike.

IV. Market Segmentation by Application

The sports medicine market is largely driven by injury type and anatomical focus, with demand concentrated in high-impact and high-frequency areas. Among these, knee-related applications dominate the market, accounting for approximately 31% of total share, reflecting the high incidence of ligament injuries (such as ACL tears), cartilage damage, and overuse conditions. The knee remains one of the most vulnerable joints in both professional and recreational sports, making it a primary focus for surgical intervention, bracing, and rehabilitation solutions.

Hip-related treatments represent the second-largest segment at around 24%, supported by increasing procedure volumes in hip arthroscopy and joint preservation techniques. Growth in this segment is also being driven by aging yet active populations seeking to maintain mobility and delay more invasive procedures such as total joint replacement.

The back and spine segment, accounting for approximately 18% of the market, reflects the growing prevalence of chronic pain, posture-related issues, and sports-induced spinal injuries. This segment extends beyond acute injuries into long-term management, including physical therapy, pain management, and minimally invasive interventions.

Shoulder injuries, which represent roughly 9% of the market, are particularly common in sports involving repetitive overhead motion—such as baseball, tennis, and swimming. Demand in this segment is supported by advancements in rotator cuff repair techniques and arthroscopic procedures.

Smaller but still meaningful segments include elbow and wrist (7%) and ankle and foot (5%), which are often associated with sport-specific injuries and acute trauma. While these categories represent a lower share of the overall market, they offer specialized opportunities for targeted devices and rehabilitation protocols.

The remaining 6% categorized as “other” includes a range of less common or multi-site injuries, as well as emerging treatment areas.

Overall, the application landscape highlights a clear concentration of value in large joint segments, particularly knees and hips, which together account for more than half of the market. This concentration underscores the importance of procedure volume, technological innovation, and clinical outcomes in driving growth, while also pointing to opportunities in specialized and underserved niches.

V. Sports Medicine Competitive Landscape

The sports medicine market operates within a complex and interconnected ecosystem, where value is distributed across device manufacturers, bracing and support providers, implant specialists, and regulatory bodies. This multi-layered structure reflects the breadth of the market, spanning everything from acute surgical intervention to long-term recovery and performance support.

At the core of the ecosystem are leading orthopedic and surgical device manufacturers such as Stryker, Arthrex, DePuy Synthes, and CONMED. These players dominate high-value segments including arthroscopy, joint repair, and minimally invasive surgical technologies, benefiting from strong surgeon relationships, extensive product portfolios, and continuous innovation.

Complementing these are bracing and support solution providers, including Enovis, Bauerfeind, Zimmer Biomet, and Ottobock, which play a critical role in non-surgical treatment, injury prevention, and post-operative rehabilitation. As the market increasingly shifts toward outpatient care and recovery optimization, this segment is gaining importance as a driver of recurring revenue and patient engagement.

On the implant side, companies such as Zimmer Biomet, BREG, and RTI Surgical are key contributors, focusing on joint reconstruction, biologics, and soft tissue repair solutions. These players operate in some of the most technically advanced and regulated areas of the market, where clinical efficacy and product reliability are critical differentiators.

Overseeing the entire ecosystem are regulatory bodies, most notably the FDA, which play a central role in shaping market entry, product innovation timelines, and compliance standards. Regulatory approval remains a key barrier to entry, reinforcing the competitive advantages of established players with proven track records.

Across this ecosystem, competition is increasingly defined by:

Integration across the care continuum (surgery → recovery → prevention)

Product innovation and clinical differentiation

Ability to scale within outpatient and ambulatory settings

Strategic positioning within high-growth niches such as biologics and rehabilitation

Importantly, the market remains fragmented despite the presence of large incumbents, creating opportunities for platform consolidation and vertical integration. Companies that can effectively combine devices, implants, and recovery solutions are best positioned to capture long-term value as sports medicine continues to evolve toward a more holistic, patient-centered model.

VI. Conclusion

The global sports medicine market is transitioning from a specialized segment into a core pillar of modern healthcare, driven by powerful and sustained structural trends. Rising participation in sports and fitness, coupled with aging yet active populations, is expanding the demand for both acute injury treatment and long-term mobility solutions.

At the same time, the market is being reshaped by rapid advancements in minimally invasive surgery, regenerative medicine, and data-driven rehabilitation, which are improving clinical outcomes while enhancing patient experience. These innovations are not only increasing the effectiveness of care, but also broadening the scope of sports medicine into prevention, performance optimization, and continuous health management.

From a market perspective, strong growth fundamentals are evident across regions, applications, and care settings. While North America continues to lead in terms of scale and innovation, emerging markets are becoming increasingly important contributors to future expansion. Similarly, high-value segments such as knee and hip treatments remain central to market growth, while adjacent areas like rehabilitation and biologics present additional upside.

The competitive landscape further reinforces the market’s potential. A mix of established global players and specialized providers, combined with ongoing fragmentation, creates a favorable environment for consolidation, platform strategies, and innovation-led differentiation. Companies that can integrate solutions across the care continuum—from surgery to recovery—are likely to capture disproportionate value.

Looking ahead, the evolution of sports medicine will be defined by its ability to adapt to changing patient expectations, technological disruption, and shifting healthcare delivery models. As the focus moves toward faster recovery, improved outcomes, and personalized care, the market is poised not only for continued expansion, but for long-term structural transformation.

For investors, operators, and healthcare stakeholders, sports medicine represents a compelling opportunity at the intersection of healthcare, technology, and consumer-driven demand—with significant room for growth, innovation, and value creation in the years ahead.

Sources and References:

Fortune Business Insights — Sports Medicine Market Analysis & Growth Outlook

Grand View Research — Sports Medicine Industry Trends & Segmentation

Precedence Research — Sports Medicine Market Size, Share & Forecast