- Healthcare 150

- Posts

- Margin Pressure Is No Longer a Sector Story. It Is a Business Model Story.

Margin Pressure Is No Longer a Sector Story. It Is a Business Model Story.

The latest survey data makes one point unmistakably clear: healthcare is not facing a uniform margin environment. It is separating into winners, survivors, and businesses under real operating pressure.

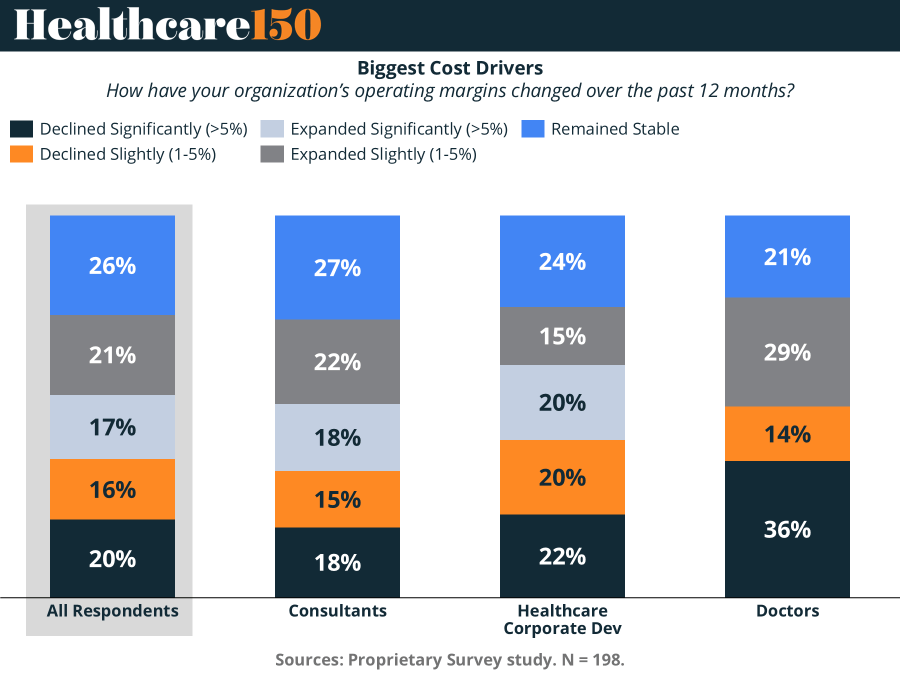

Across all respondents, the market looks almost evenly split at first glance. 38% reported margin expansion over the past 12 months, including 21% who expanded slightly and 17% who expanded significantly. On the other side, 36% reported margin decline, with 16% declining slightly and 20% declining significantly. Another 26% said margins remained stable. That topline picture suggests a sector still capable of producing resilience, but it also shows how uneven that resilience has become.

The real signal sits in the subgroup data.

Doctors are carrying the most visible margin stress. Among physician respondents, 36% said margins declined significantly, by far the highest figure of any cohort in the survey. Another 14% reported slight decline, taking total contraction to 50%. Only 29% reported slight expansion, and just 21% said margins were stable. Notably, there is no visible meaningful share of doctors reporting significant expansion. That is a stark result. It points to a provider economy still squeezed by labor inflation, staffing shortages, rising non-clinical overhead, and reimbursement frameworks that do not move fast enough to absorb cost growth.

For investors and acquirers, that matters. A physician-heavy platform may still show volume growth and revenue momentum, but that is no guarantee of earnings quality. When one in three doctors reports significant margin deterioration, the underwriting question becomes less about top-line demand and more about how much of the operating model can realistically be fixed.

Consultants sit at the opposite end of the spectrum. In that group, only 18% reported significant decline and 15% reported slight decline, for total contraction of 33%. By contrast, 40% reported margin expansion, including 22% with slight expansion and 18% with significant expansion. Another 27% remained stable. This is the cleanest resilience profile in the survey. Advisory businesses continue to benefit from pricing flexibility, lower fixed-cost intensity, and a cost base that can be adjusted faster than provider organizations can adjust theirs. In practical terms, these businesses have more room to protect profitability when wage and operating inflation remain elevated.

Healthcare corporate development respondents land in the middle, but not comfortably. Here, 22% reported significant decline and 20% slight decline, meaning 42% experienced margin compression. At the same time, 35% reported expansion, split between 15% slight expansion and 20% significant expansion, while 24% remained stable. That distribution reflects a mixed operating reality. Scale, centralization, and portfolio diversification can create buffers, but they do not eliminate exposure to labor costs, supply inflation, and pressure on reimbursement-linked businesses. The group is not in crisis, but neither is it insulated.

The broader implication is straightforward. The closer a business is to frontline care delivery, the harder it is to protect margin. The farther it is from labor-intensive clinical operations, the more room it has to preserve economics through pricing, utilization management, and operating flexibility.

That divide should now shape strategy.

For management teams, small-bore cost initiatives are unlikely to be enough. The businesses holding the line are likely doing several things at once: redesigning labor models, tightening revenue cycle execution, pruning lower-yield service lines, and pushing much harder on productivity. The 26% of all respondents who maintained stable margins are important because they represent operational discipline in a difficult environment, not a neutral outcome.

The headline is not that healthcare margins are collapsing. The headline is that margin performance is diverging sharply by model, and that divergence is now central to valuation, diligence, and strategic positioning.