- Healthcare 150

- Posts

- Healthcare’s Margin Playbook Is Getting More Selective

Healthcare’s Margin Playbook Is Getting More Selective

Margin protection in healthcare used to mean one thing: cut costs faster than revenue slows.

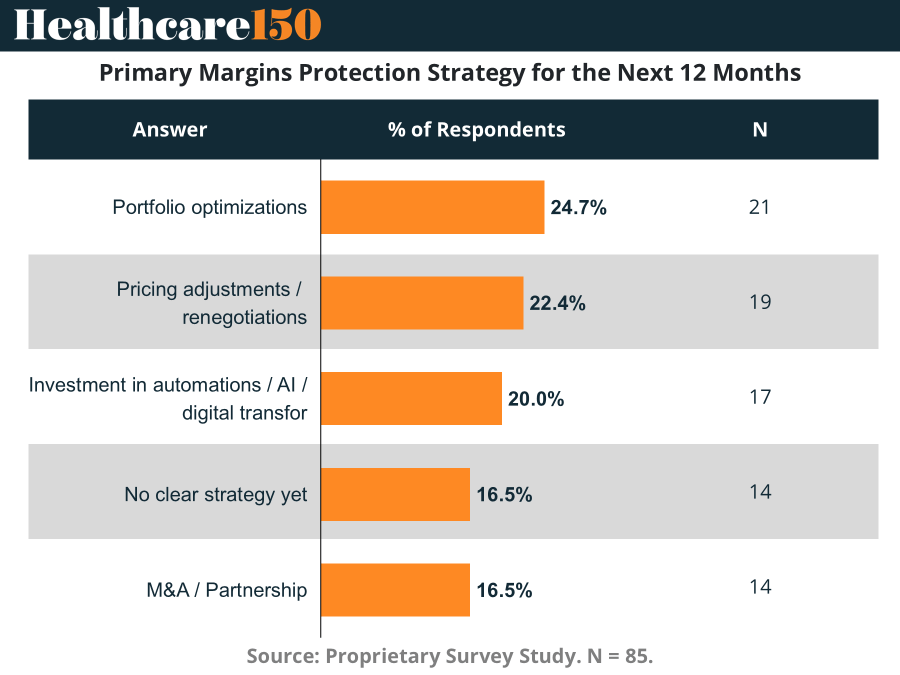

Margin protection in healthcare used to mean one thing: cut costs faster than revenue slows. That playbook is evolving. In our latest proprietary survey of healthcare executives, investors, consultants, and corporate development leaders, the top strategy for protecting margins over the next 12 to 24 months was not layoffs or blanket expense reductions. Instead, 24.7% of respondents pointed to portfolio optimization as their primary focus. That shift matters.

Healthcare operators are increasingly realizing that not every service line, product category, or market deserves equal attention. In a higher rate environment where labor costs remain elevated and reimbursement pressure persists, the emphasis is moving toward concentration rather than expansion. Companies are becoming more disciplined about where they allocate capital and management attention.

Translation: healthcare firms are starting to prioritize quality of revenue over quantity of revenue.

The second most common response, at 22.4%, was pricing adjustments and renegotiations. That reflects the reality facing much of the industry today. Hospitals, providers, medtech firms, and healthcare services businesses continue operating in a market where input costs climbed faster than reimbursement structures adapted.

For many organizations, margin recovery increasingly depends on renegotiating contracts with payers, suppliers, and commercial partners rather than simply driving higher volume.

That dynamic is particularly important for private equity backed healthcare assets. Sponsors underwriting deals during the lower rate era often assumed operational efficiencies alone could offset inflationary pressures. Today, pricing power is becoming a more central part of the investment thesis.

Meanwhile, 20.0% of respondents identified automation, AI, and digital transformation as their primary strategy.

That result highlights a broader shift happening across healthcare. Technology investments are no longer viewed purely as growth initiatives or innovation experiments. They are becoming operational necessities.

From revenue cycle automation to AI assisted clinical workflows and administrative efficiency tools, healthcare organizations increasingly see technology as a structural margin lever. The objective is not simply reducing headcount. It is improving throughput, reducing friction, and preserving operating leverage in an environment where labor shortages remain persistent.

Importantly, the survey also revealed fragmentation in how organizations are approaching the problem.

While some firms are pursuing targeted portfolio rationalization and technology driven efficiency, 16.5% of respondents said they still have no clear strategy in place.

That uncertainty may prove costly.

Healthcare sits in a uniquely difficult operating environment. Costs remain sticky, reimbursement timelines are slow to adjust, and regulatory complexity continues increasing across multiple subsectors. Unlike prior cycles, firms cannot rely solely on market growth to protect profitability.

The organizations that outperform over the next several years will likely be the ones that combine operational discipline with strategic clarity.

For investors, the implications are equally important.

The healthcare businesses most likely to command premium valuations going forward may not necessarily be the fastest growing assets. Instead, buyers may increasingly reward companies with durable pricing power, focused portfolio strategies, scalable technology infrastructure, and visible operational resilience.