- Healthcare 150

- Posts

- Europe’s Healthcare Reset: Cost Pressure, Digital Investment, and the Shift Beyond Hospitals

Europe’s Healthcare Reset: Cost Pressure, Digital Investment, and the Shift Beyond Hospitals

European healthcare systems are entering a decisive period of structural change.

Aging populations, workforce shortages, rising treatment costs, and persistent fiscal pressure are forcing health systems to rethink how care is delivered and financed. Traditional models built around hospital-centric care and expanding public budgets are increasingly difficult to sustain. As a result, healthcare leaders across Europe are searching for new ways to improve efficiency without compromising quality or access.

A clear pattern is emerging: operational transformation is becoming the primary strategy for navigating financial constraints. Health systems are increasingly turning to automation, predictive analytics, and digital infrastructure to streamline workflows, optimize staffing, and reduce unnecessary utilization. At the same time, technology investment is shifting away from experimentation toward foundational capabilities such as core clinical systems, cybersecurity, and data modernization that can support long-term digital transformation.

Alongside these operational changes, the structure of care delivery itself is evolving. Spending patterns across Europe suggest a gradual transition away from hospital-dominated systems toward more distributed models that emphasize outpatient services, preventive care, and community-based providers. Meanwhile, the financing foundations of European healthcare remain largely collective, with compulsory insurance and public funding continuing to underpin system sustainability.

Taken together, these trends point to a broader transformation underway across the European healthcare landscape. Efficiency is no longer simply a matter of cost reduction. It increasingly depends on redesigning workflows, investing in digital infrastructure, and shifting care delivery to more scalable and accessible settings.

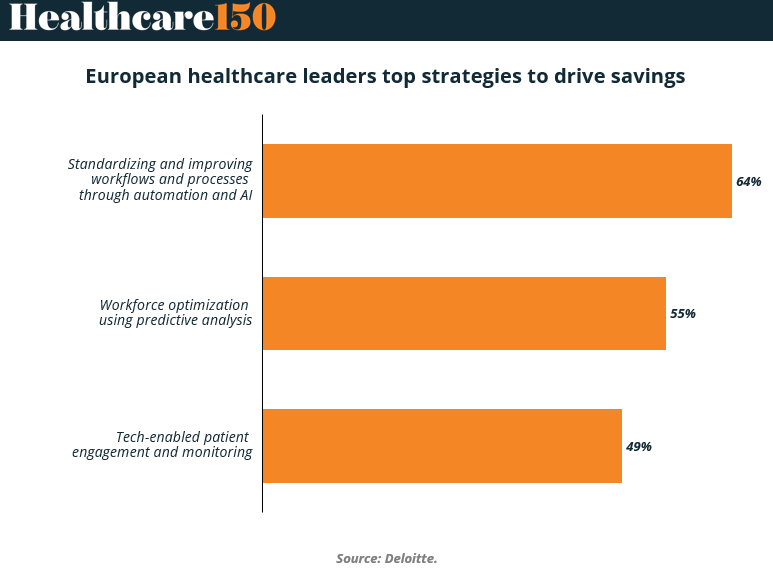

European Healthcare Leaders Top Strategies to Drive Savings

European health systems are entering a period of sustained financial pressure. Aging populations, workforce shortages, and rising treatment costs are pushing providers to rethink how efficiency is achieved across care delivery. Rather than relying solely on cost cutting, leaders are increasingly pursuing structural changes that improve operational productivity while maintaining clinical quality.

The data highlights a clear priority: operational transformation through automation and analytics. Standardizing workflows and improving processes through automation and AI leads the list at 64%, indicating that hospitals see the greatest savings potential in reducing administrative friction and eliminating manual processes.

Workforce optimization using predictive analysis follows at 55%, reflecting the growing need to better allocate scarce clinical staff and manage scheduling, staffing levels, and patient flow more effectively. Technology-enabled patient engagement and monitoring ranks third at 49%, showing that digital tools are also being viewed as cost-control mechanisms, particularly in chronic care and post-discharge management.

Taken together, the strategies reflect a shift in how European providers approach cost management. The focus is no longer purely on procurement or budget reductions but on redesigning how care systems operate. Automation, predictive analytics, and digital monitoring tools are increasingly viewed as infrastructure for financial sustainability rather than experimental innovation.

Key takeaways from chart

Automation and AI dominate cost strategies (64%), highlighting how administrative complexity and fragmented workflows remain major cost drivers across European healthcare systems.

Workflow standardization signals operational maturity, as health systems move beyond isolated digital pilots toward enterprise-wide process redesign.

Workforce optimization (55%) reflects structural staffing shortages, particularly across nursing, diagnostics, and administrative support roles.

Predictive analytics is becoming a planning tool, allowing hospitals to forecast patient volumes, staffing needs, and operational bottlenecks.

Tech-enabled patient engagement (49%) is emerging as a cost lever, especially in remote monitoring and chronic disease management where early intervention can reduce hospital utilization.

The convergence of automation, analytics, and digital monitoring suggests a platform-driven future, where operational data flows across clinical, administrative, and patient-facing systems.

For investors and healthtech vendors, the signal is clear: solutions that directly reduce operational friction or improve workforce efficiency are most aligned with current provider priorities.

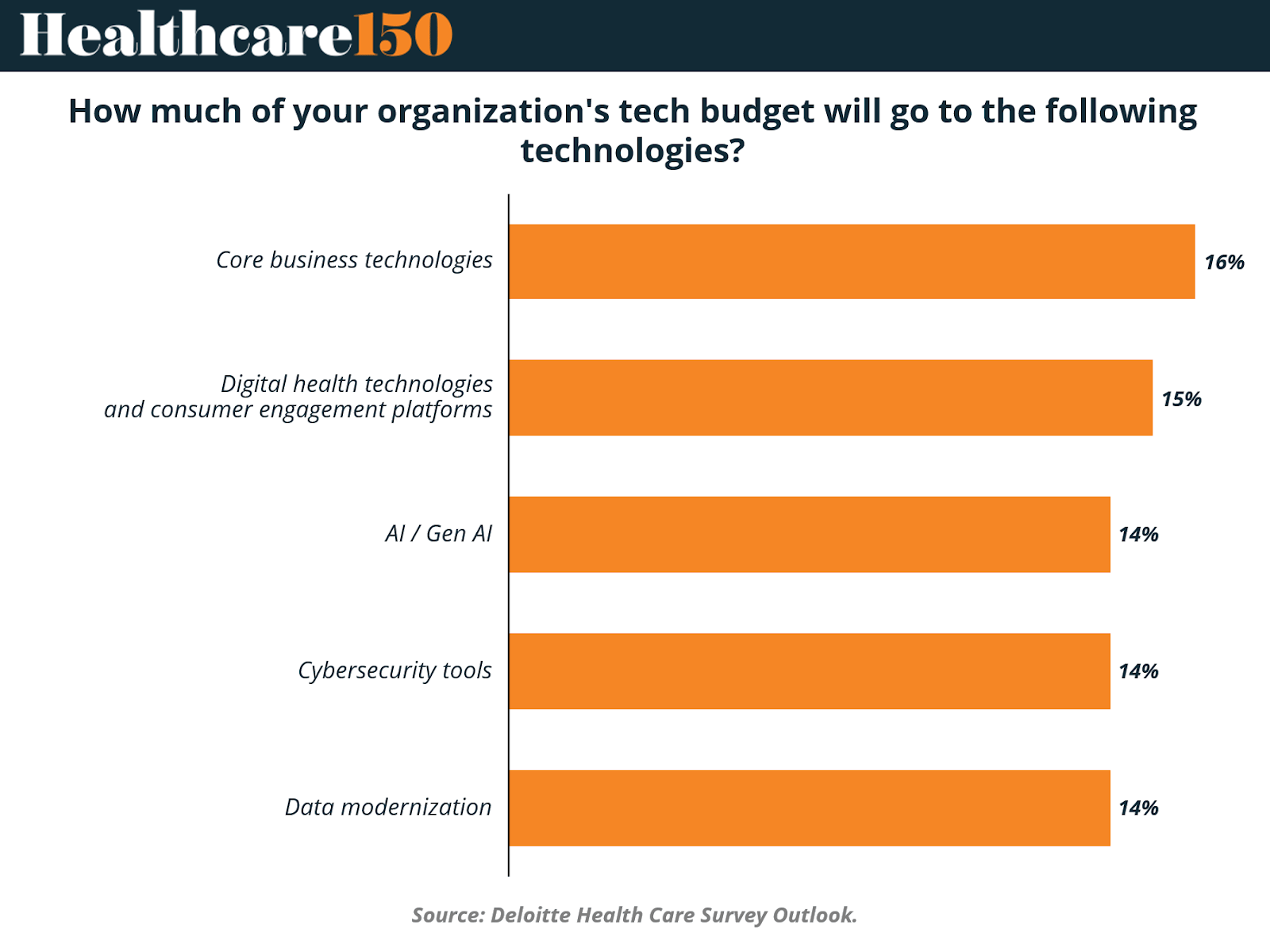

Allocation of Healthcare Technology Budgets in European Organizations

Healthcare organizations across Europe are shifting from experimental digital investments toward more balanced and operationally focused technology spending. After several years of rapid innovation cycles driven by the pandemic and digital health expansion, providers are now prioritizing technologies that strengthen the core infrastructure of care delivery while still enabling future innovation.

The data reflects a relatively even distribution of investment across several technology categories, with core business technologies receiving the largest share at 16% of total tech budgets. This suggests that hospitals and health systems are prioritizing foundational systems such as electronic health records, enterprise platforms, and operational software that support day-to-day clinical and administrative workflows.

Close behind are digital health technologies and consumer engagement platforms at 15%, reflecting continued investment in patient-facing tools, virtual care platforms, and digital communication systems.

Artificial intelligence, cybersecurity, and data modernization each account for 14% of technology budgets, highlighting how healthcare organizations increasingly view these capabilities as essential infrastructure rather than niche investments. Together, the allocation indicates that European healthcare leaders are pursuing a balanced technology strategy. They are strengthening core systems while simultaneously building the data, security, and AI capabilities required to support next-generation care delivery models.

Key takeaways from chart

Core business technologies command the largest share of investment (16%), underscoring the need to modernize foundational systems such as EHRs, operational software, and clinical workflow platforms.

Digital health and patient engagement tools (15%) remain a major priority, reflecting continued emphasis on improving access, communication, and remote care delivery.

AI and generative AI represent a significant but measured investment (14%), suggesting that healthcare organizations are moving cautiously from pilot experimentation toward operational deployment.

Cybersecurity investment (14%) reflects growing regulatory and operational risk, particularly as health systems expand digital infrastructure and patient data exchange.

Data modernization (14%) signals recognition that advanced analytics and AI depend on robust data architecture, including interoperable systems, real-time data pipelines, and scalable cloud infrastructure.

The narrow spread across categories suggests diversification rather than concentration, indicating that healthcare organizations see digital transformation as a multi-layered challenge requiring coordinated investment across infrastructure, analytics, and patient-facing platforms.

For technology vendors and investors, the opportunity lies in integrated platforms, as health systems increasingly prefer solutions that connect core systems, data infrastructure, and AI capabilities rather than isolated tools.

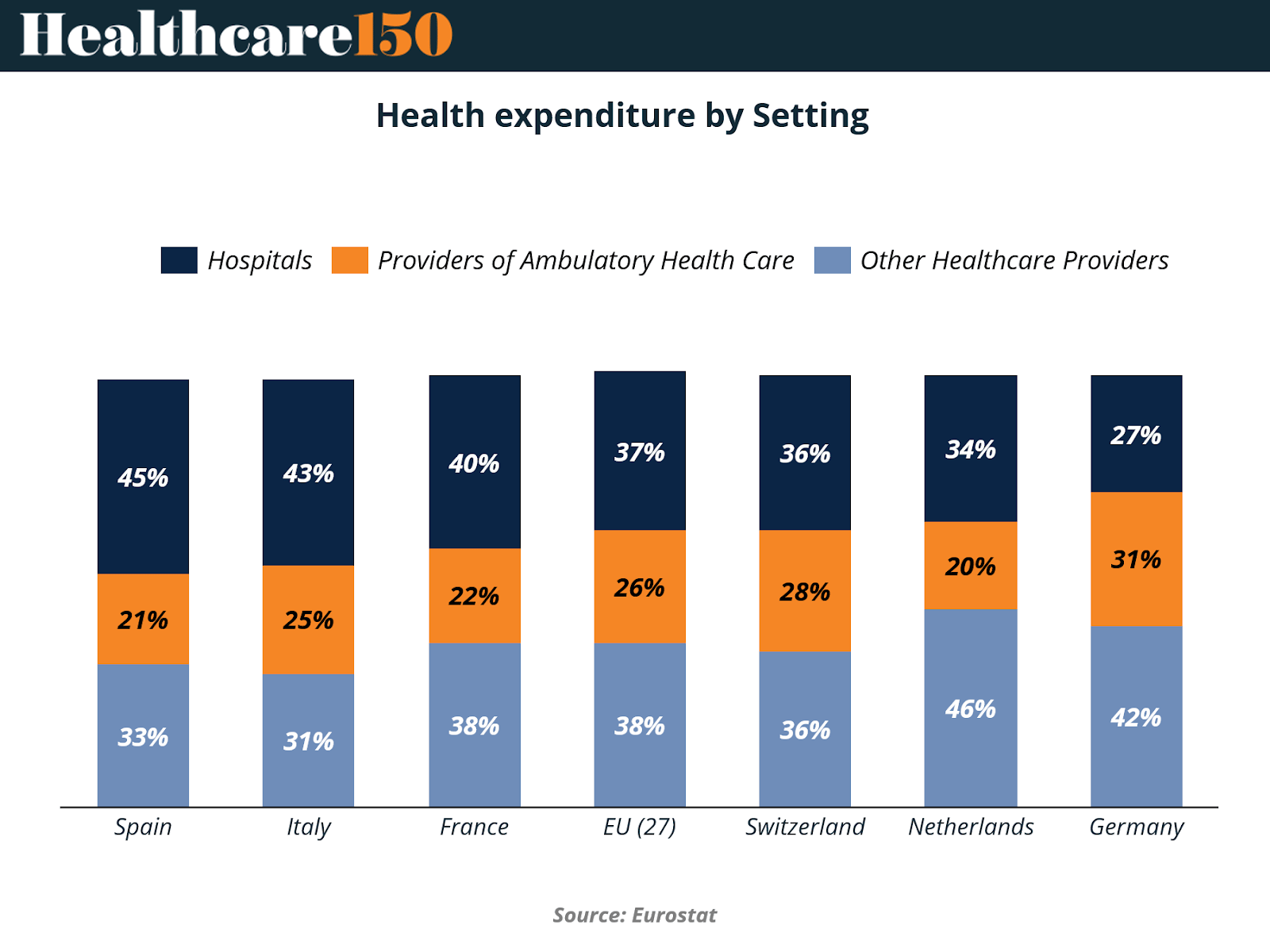

Health Expenditure by Care Setting Across Selected European Countries

European healthcare systems allocate spending differently depending on how care is delivered. While hospitals historically dominated healthcare expenditure, many countries are gradually shifting resources toward outpatient and community-based services as systems aim to reduce inpatient costs and manage growing demand more efficiently.

The chart highlights significant variation across European markets. In Spain and Italy, hospitals still account for the largest share of health spending at 45% and 43%, respectively, indicating systems that remain heavily hospital-centered. In contrast, countries such as the Netherlands and Germany show a more diversified distribution of spending.

The Netherlands allocates 46% of health expenditure to other healthcare providers, while Germany directs 31% toward ambulatory care services, signaling a stronger emphasis on decentralized care delivery.

Overall, the EU average allocates 37% of health expenditure to hospitals, 26% to ambulatory providers, and 38% to other healthcare providers, reflecting a gradual transition toward more distributed care models. As healthcare demand rises and cost pressures intensify, many European systems are exploring ways to move care outside hospital settings, leveraging outpatient networks, preventive services, and specialized providers to improve efficiency and patient outcomes.

Key Takeaways from Chart

Hospital spending remains dominant in Southern Europe, with Spain (45%) and Italy (43%) allocating the largest shares of health expenditure to inpatient care.

Northern and Western European systems show greater diversification, with the Netherlands allocating 46% of spending to other healthcare providers and Germany allocating 42% to this category.

Ambulatory care spending is highest in Germany at 31%, suggesting a stronger reliance on outpatient physician networks and community-based treatment models.

The EU average reflects a transitional model, where hospitals still command the largest single share (37%), but non-hospital providers collectively represent a growing portion of care delivery.

Countries with stronger outpatient ecosystems tend to shift resources away from hospitals, improving system flexibility and reducing reliance on expensive inpatient services.

The Netherlands stands out for its lower hospital share (34%), reflecting a healthcare structure that emphasizes primary care coordination and community-based services.

For policymakers and health system leaders, the data underscores a broader structural shift, as many European systems seek to rebalance spending toward outpatient care, prevention, and integrated service delivery models.

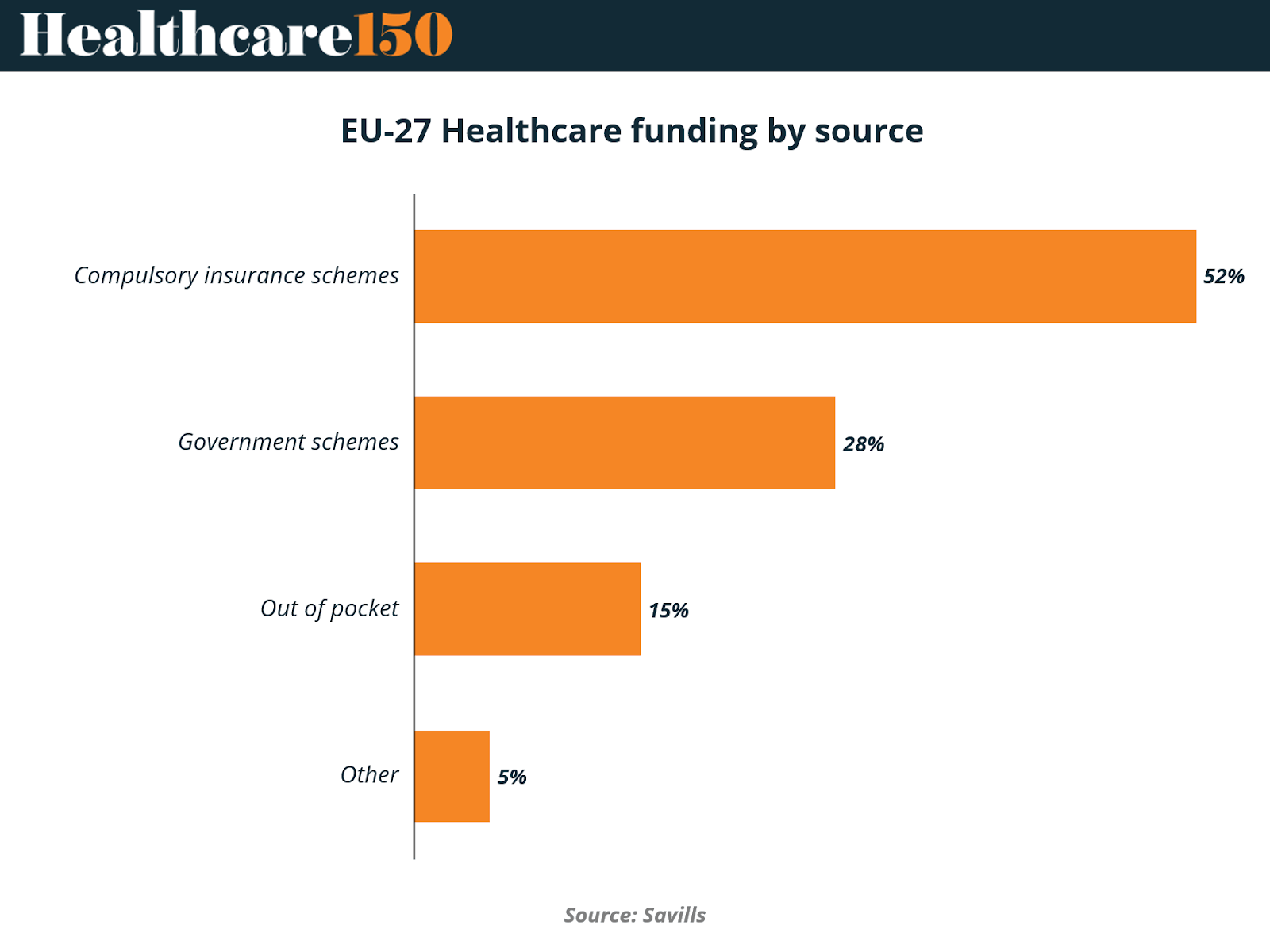

EU-27 Healthcare Funding by Source

Healthcare systems across the European Union rely on a mix of public financing, insurance-based contributions, and direct patient payments. While individual national models differ, the broader EU framework reflects a hybrid structure where compulsory insurance and government funding together form the backbone of healthcare financing.

The chart highlights the dominant role of insurance-based funding mechanisms across the EU-27. Compulsory insurance schemes account for 52% of total healthcare funding, making them the largest source of financing. These schemes, typically funded through payroll contributions shared by employers and employees, are a central feature of many European health systems, particularly in countries such as Germany, France, and the Netherlands. Government schemes represent 28% of healthcare funding, reflecting the continued role of tax-based public financing that supports national health systems, public hospitals, and broader population health initiatives.

Private contributions remain comparatively limited but still significant. Out-of-pocket spending represents 15% of healthcare financing, while other sources contribute 5%. Although these shares are smaller, they often include payments for services not fully covered by public systems, such as elective procedures, dental care, or specialized treatments. Overall, the data illustrates how European healthcare remains primarily publicly financed, with compulsory insurance acting as the central financial pillar across the EU.

Key Takeaways from chart

Compulsory insurance schemes dominate EU healthcare financing (52%), reflecting the widespread adoption of social health insurance models across many European countries.

Government-funded healthcare accounts for 28%, supporting national health systems, public hospitals, and population health programs funded through taxation.

Public and compulsory financing together represent roughly 80% of healthcare funding, underscoring the strong role of collective financing mechanisms in European healthcare.

Out-of-pocket spending remains relatively moderate at 15%, significantly lower than levels seen in many other global healthcare systems.

The limited role of private funding helps protect access and affordability, reducing the financial burden on patients for essential healthcare services.

Countries with strong insurance-based systems tend to balance public oversight with decentralized financing, enabling flexibility while maintaining broad coverage.

For policymakers, the funding mix highlights the importance of maintaining sustainable insurance contributions, particularly as aging populations and rising treatment costs place increasing pressure on healthcare budgets.

Conclusion

The data across these charts highlights a healthcare system in transition. European providers are responding to growing financial pressure not through isolated cost-cutting initiatives, but through structural changes that reshape how care is organized, delivered, and financed.

Operational efficiency has become the central priority. Automation, predictive analytics, and digital engagement tools are being deployed to streamline workflows, manage workforce shortages, and reduce administrative complexity. At the same time, technology investment is becoming more strategic and infrastructure-focused, with organizations strengthening core systems, data architecture, and cybersecurity capabilities that will support future innovation.

Equally important is the ongoing shift in care delivery models. Spending patterns across Europe suggest that health systems are gradually moving away from hospital-centered care toward more decentralized networks that rely on outpatient providers, preventive services, and community-based care. These changes are driven by both economic necessity and the need to better manage chronic disease and aging populations.

Despite these operational shifts, the financial foundations of European healthcare remain largely stable. Compulsory insurance schemes and public funding continue to provide the majority of system financing, helping preserve access and affordability across the region.

Looking ahead, the success of European healthcare systems will likely depend on how effectively they can align these three forces: operational transformation, digital infrastructure investment, and structural changes in care delivery. Together, they represent the key levers through which healthcare leaders are attempting to build more sustainable, resilient systems for the decade ahead.

Sources & References

Deloitte. 2026 Global Health Care Outlook. https://www.deloitte.com/us/en/insights/industry/health-care/life-sciences-and-health-care-industry-outlooks/2026-global-health-care-outlook.html

Euronews. Digital Health Across Europe. https://www.euronews.com/health/2026/02/23/digital-health-across-europe-which-country-leads-acess-to-electronic-health-records-and-li

Savills. UK and European Hospitals Spotlight. https://www.savills.co.uk/research_articles/229130/388244-0/uk-and-european-hospitals-spotlight---q1-2026

NCH Stats. EU vs Europe. https://nchstats.com/us-vs-europe-healthcare/