- Healthcare 150

- Posts

- 80% of CEOs Are Shifting Strategy—Here’s Why

80% of CEOs Are Shifting Strategy—Here’s Why

From Caution to Reinvention — What’s Driving the CEO Reset

Good morning, ! Today diving into the key cost drivers shaping companies, why nearly 80% of healthcare CEOs are increasing investment in portfolio transformation, and Cencora’s $1.1B acquisition of EyeSouth’s retina business.

Want to advertise in Healthcare 150? Check out our ad platform, here.

Know someone in the healthcare space who should see this? Forward it their way. Here’s the link.

— The Healthcare150 Team

MICROSURVEY

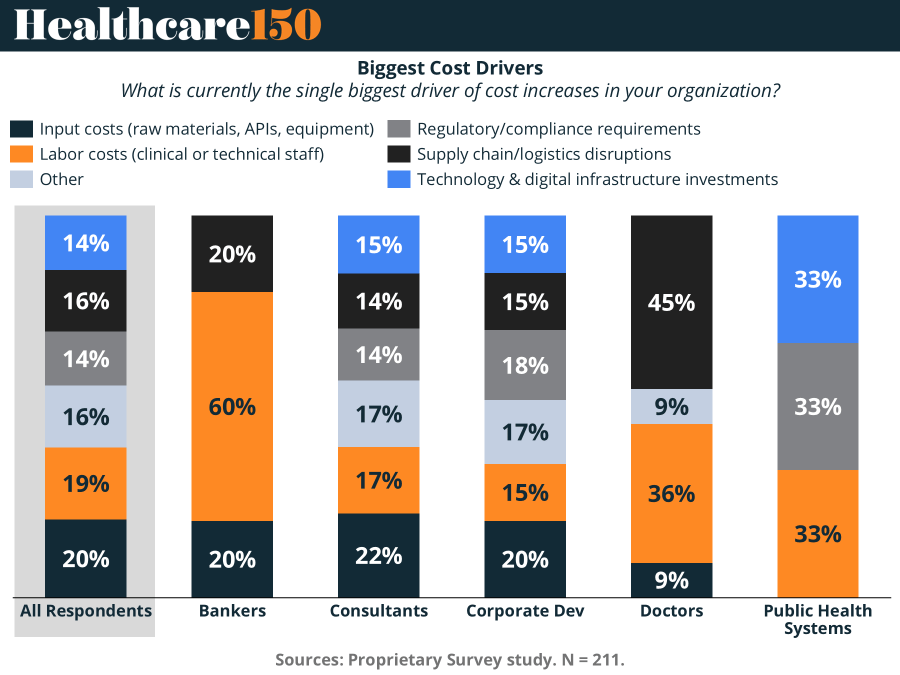

What’s Really Driving Healthcare Costs?

Our microsurvey from last week reveals a clear message: cost pressure in healthcare is broad, not concentrated. The top drivers, input costs (20%) and labor (19%), are closely followed by supply chain disruptions (16%), regulation (14%), and technology investments (14%). No single factor dominates, pointing to a multifactorial cost environment.

Importantly, over 90% of respondents come from consulting (62.6%) and corporate development (28.4%). This makes the overall distribution a strong, system-level signal, reflecting cross-functional visibility rather than narrow operational bias. Their balanced responses reinforce that cost pressures are structural and widespread.

That said, differences matter. Doctors highlight supply chain (45%) and labor (36%), while bankers overwhelmingly point to labor (60%). Meanwhile, public health systems face a three-way pressure across labor, regulation, and technology (33% each). (More)

HEADLINE OF THE WEEK

M&A Integration Becomes the Real Value Driver

Healthcare M&A is shifting from dealmaking to delivery. Nearly 80% of healthcare CEOs plan to increase investment in portfolio transformation, with 69% prioritizing financial performance, signaling that integration, not acquisition, is now the primary value lever.

The distinction is structural. Traditional integrations focused on cost synergies and speed. Transformational integrations are multi-year efforts aimed at revenue growth, operating model reinvention, and clinical alignment. Timelines now stretch 4+ years, with capital intensity and execution risk rising accordingly.

This reframes how value is created. Synergies are no longer limited to overhead reduction. They include care model redesign, service line expansion, and technology-enabled coordination across payer and provider assets. The result is a broader but less certain value pool.

Execution is the constraint. Failures increasingly trace back to weak governance, insufficient planning, and underinvestment in change management rather than flawed deal logic.

Why it matters: As margins compress and organic growth slows, integration capability is becoming a core competitive advantage. The next cycle of winners will not be those who buy best, but those who integrate best. (More)

PRESENTED BY JUNIPER SQUARE

How one GP modernized operations for a more complex fund structure

As firms expand into new fund structures, increase investor counts, and face heightened reporting expectations, the operating model either scales with them or becomes the constraint.

Avanath Capital Management reached that inflection point. As their platform grew, so did the complexity across fund accounting, reporting, and investor servicing. Rather than adding more manual processes or stitching together additional systems, they modernized their infrastructure with Juniper Square.

See how Avanath:

Unified fund and investor data on a single platform

Reduced reconciliation and reporting friction

Increased visibility across teams

Strengthened the investor experience through connected operations

The outcome wasn’t just efficiency; it was operational resilience.

Supporting our sponsors supports our free newsletters. Please support our sponsors!

DEAL OF THE WEEK

Cencora Doubles Down on Retina Roll-Up

Cencora is writing another $1.1B check, this time for EyeSouth Partners’ retina business, and further cementing its push into specialty care. The assets will fold into Retina Consultants of America (RCA), its MSO platform acquired just last year for north of $4B.

Why it matters: This isn’t just tuck-in M&A—it’s a scale play in a fragmented ophthalmology market with growing exposure to biosimilars. Those therapies (particularly for diabetic retinopathy and macular degeneration) are driving volume—and margins.

Zoom out: Drug distributors are quietly becoming care enablers, not just middlemen. With peers like McKesson making similar bets, retina is starting to look like the latest roll-up battleground.

The bottom line: More scale, more specialization, and a clearer pivot toward higher-margin services. (More)

REGIONAL FOCUS

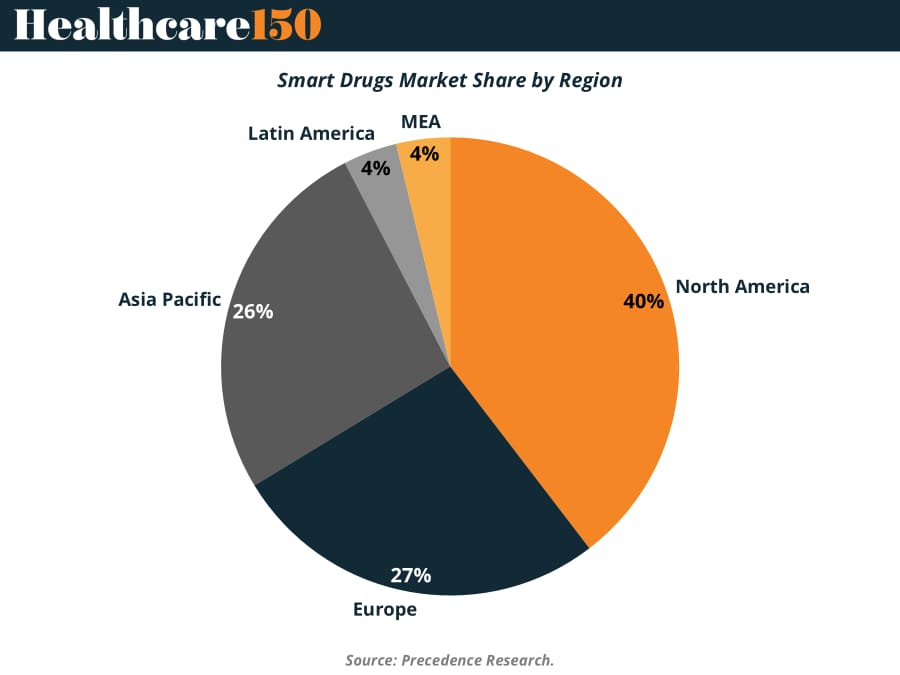

Smart Drugs Go Global, But Not Evenly

The Smart Drugs market is scaling globally, but not symmetrically.

North America (~39.6%) remains the center of gravity, driven by biotech innovation, deep clinical infrastructure, and strong demand across aging populations and high-performance users. The U.S. continues to set the pace on both commercialization and off-label adoption.

Europe (~26.7%) offers steady growth, backed by regulatory support and rising mental health awareness, though fragmentation keeps expansion measured.

Asia-Pacific (~26.1%) is the real story: nearly tied in share, but leading in growth velocity, fueled by rising healthcare spend and expanding middle classes. (More)

“Success is walking from failure to failure with no loss of enthusiasm.”

Winston Churchill